إن الفهم الواضح للوضع المالي يُعد أمرًا أساسيًا لاتخاذ قرارات مدروسة، خصوصًا عندما يتعلق الأمر بإدارة العمليات اليومية. ويُعد رأس المال العامل أحد أهم المؤشرات على الصحة المالية للشركة، حيث يوضح قدرة الشركة على تغطية التزاماتها قصيرة الأجل باستخدام مواردها المتاحة.

تضمن الإدارة السليمة لرأس المال العامل قدرة الشركات على الوفاء بمصروفاتها اليومية مع استمرار العمليات بسلاسة. في هذا المقال، سنستعرض تعريف رأس المال العامل، وأهميته في الإدارة المالية، وكيف يمكن للشركات الاستفادة منه لضمان السيولة والاستقرار المالي. كما سنوضح طريقة حسابه ومكوناته الأساسية، وكيفية إدارته بشكل فعّال لتحسين النمو وكفاءة التشغيل.

ما هو رأس المال العامل؟

رأس المال العامل هو الفرق بين الأصول المتداولة والالتزامات المتداولة للشركة. وهو يمثل الأموال المتاحة للعمليات اليومية، ويُعد مؤشرًا مهمًا على الصحة المالية قصيرة الأجل للشركة.

يعمل رأس المال العامل كوسادة مالية تضمن استمرار العمليات دون انقطاع. ويساعد توفر رأس مال عامل كافٍ الشركة على دفع فواتيرها في الوقت المناسب، والاستثمار في فرص النمو، والتعامل مع التحديات المالية غير المتوقعة بكفاءة. أما إذا كان رأس المال العامل منخفضًا جدًا، فقد تواجه الشركة صعوبات في الوفاء بالتزاماتها وقد تتعرض لمشكلات في السيولة.

من خلال فهم رأس المال العامل، يمكن للشركات قياس كفاءتها التشغيلية، ووضع السيولة لديها، واستقرارها المالي على المدى القصير. والآن، دعنا نلقي نظرة على سبب كون رأس المال العامل مؤشرًا ماليًا بالغ الأهمية.

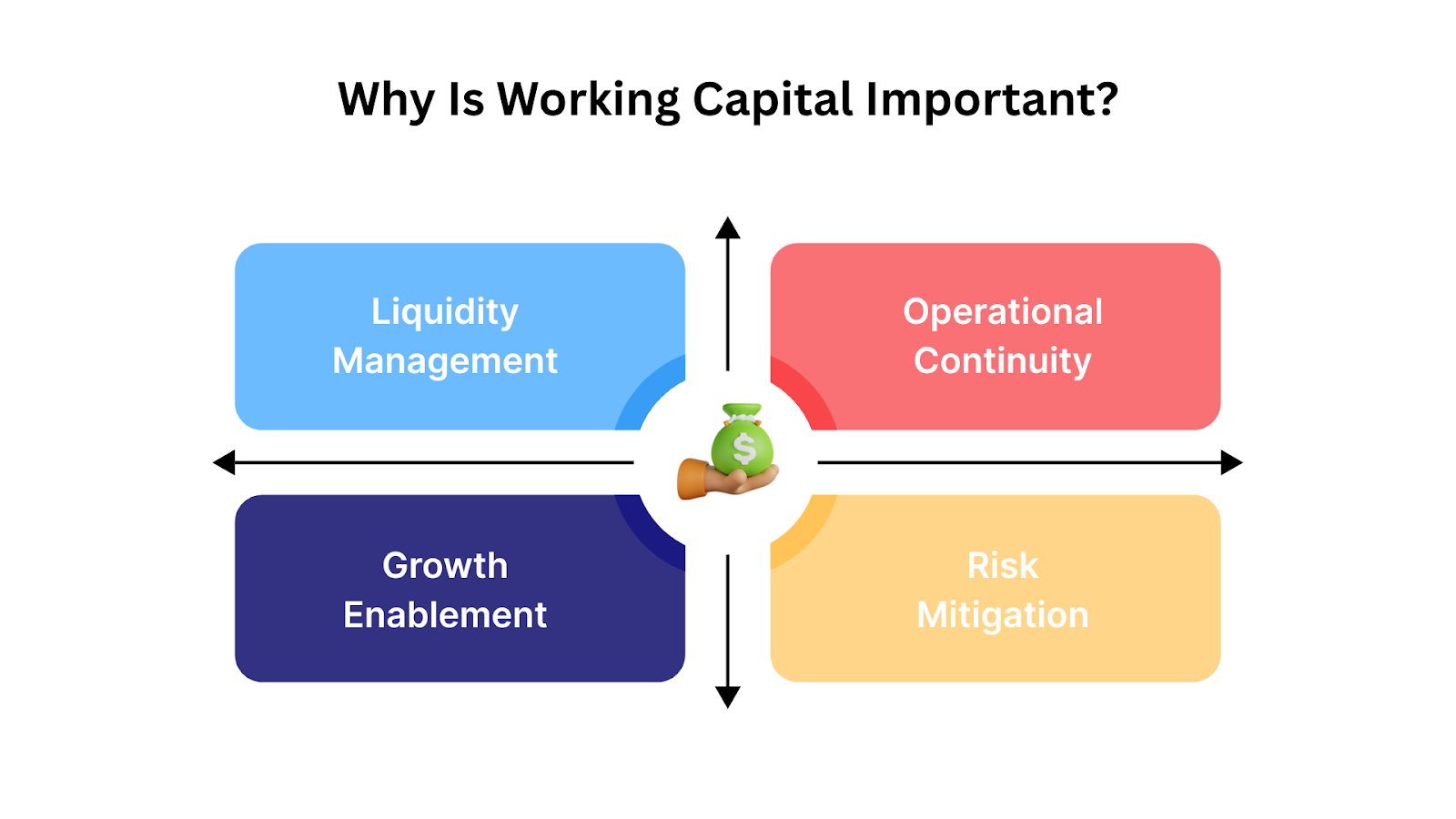

لماذا يُعد رأس المال العامل مهمًا؟

يُعد رأس المال العامل مؤشرًا ماليًا مهمًا لأنه يؤثر بشكل مباشر على سيولة الشركة وكفاءتها التشغيلية واستقرارها العام. ويوفر المستوى الصحي من رأس المال العامل عدة مزايا رئيسية:

إدارة السيولة: يضمن توفر أصول سائلة كافية لسداد الالتزامات قصيرة الأجل وتغطية المصروفات اليومية.

استمرارية العمليات: يساعد على استمرار النشاط بسلاسة من خلال توفير الأموال اللازمة لإدارة المخزون، ودفع الرواتب، وسداد مستحقات الموردين.

تقليل المخاطر: يقلل من خطر التعثر المالي من خلال ضمان قدرة الشركة على الوفاء بالتزاماتها دون تأخير.

دعم النمو: يتيح الاستثمار في مشاريع وفرص جديدة عبر توفير مرونة مالية أكبر.

ومع الإدارة الجيدة، يمكن تحسين رأس المال العامل ليصبح أداة فعّالة تدعم توسّع الأعمال. وفي الخطوة التالية، سنستعرض مزايا الحفاظ على مستويات صحية من رأس المال العامل.

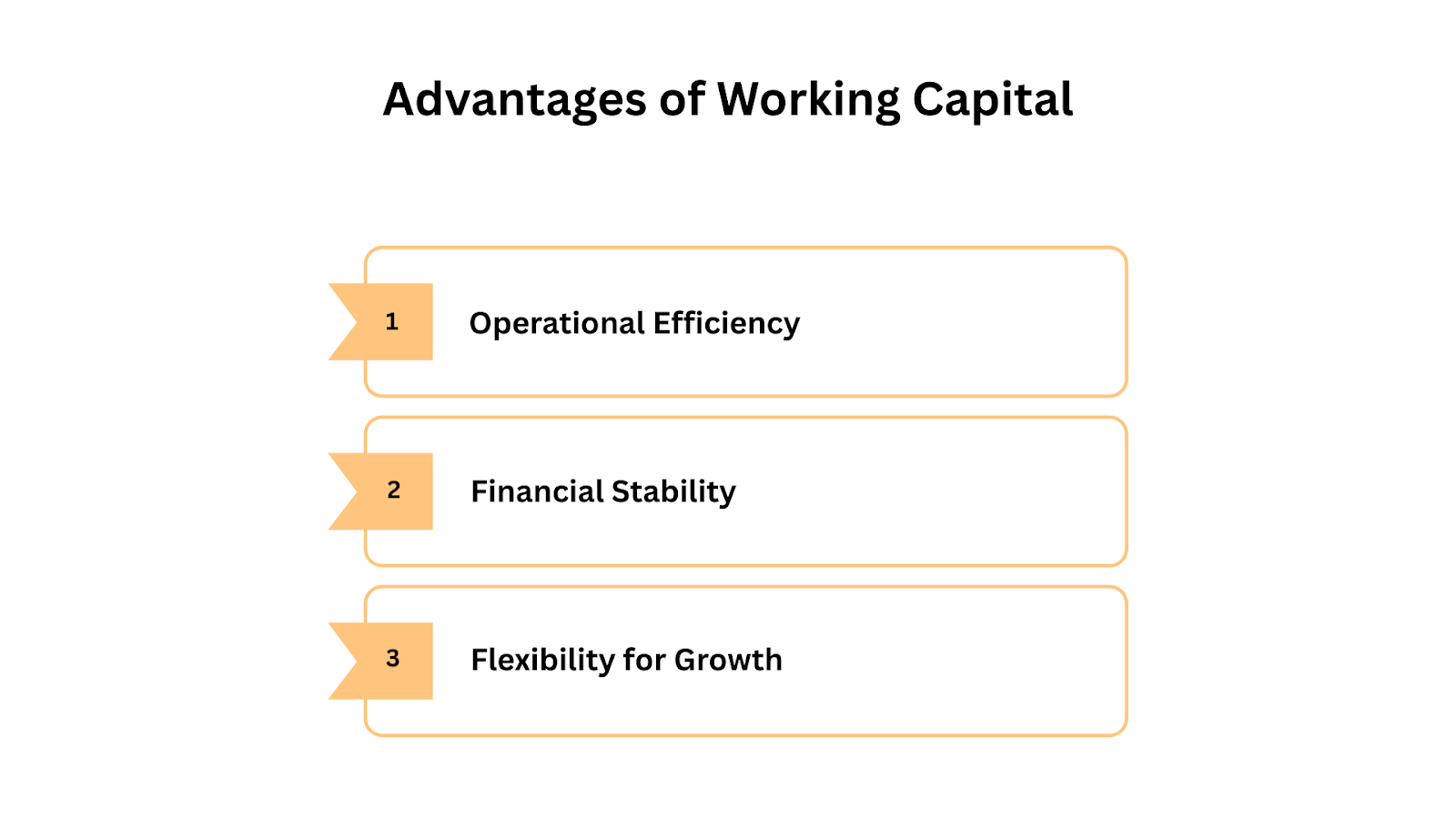

مزايا رأس المال العامل

يوفر وجود مستوى مناسب من رأس المال العامل العديد من المزايا التي تضمن الاستقرار المالي والنجاح التشغيلي، ومنها:

الكفاءة التشغيلية: يتيح للشركة تغطية المصاريف اليومية مثل الإيجارات، الخدمات، والرواتب دون انقطاع، مما يضمن سير العمل بسلاسة.

الاستقرار المالي: يقلل من مخاطر مشاكل التدفق النقدي، ويساعد على إدارة الديون قصيرة الأجل وتجنب الضغوط المالية خلال فترات التباطؤ أو الأزمات الاقتصادية.

المرونة في النمو: يمكّن الشركات من اغتنام فرص التوسع، مثل زيادة المخزون أو الاستثمار في التسويق، دون التأثير على الالتزامات قصيرة الأجل.

فعلى سبيل المثال، يمكن لمتجر ملابس موسمي شراء مخزون إضافي قبل موسم الذروة لضمان تلبية الطلب مع الحفاظ على استقرار عملياته اليومية.

وبتحقيق هذا التوازن، تستطيع الشركات الحفاظ على الاستقرار والاستعداد لكل من الاحتياجات قصيرة المدى وفرص النمو طويلة المدى.

ومع هذه الفوائد، دعنا ننتقل إلى كيفية ارتباط رأس المال العامل بالميزانية العمومية.

دور الميزانية العمومية في حساب رأس المال العامل

يُشتق رأس المال العامل من عناصر موجودة في الميزانية العمومية للشركة، وتحديدًا الأصول المتداولة والالتزامات المتداولة. وتُعد الميزانية العمومية، إلى جانب قائمة الدخل وقائمة التدفقات النقدية، من أهم القوائم المالية التي تُستخدم لتقييم أداء الشركة.

وعلى عكس القوائم المالية الأخرى التي تعكس الأداء خلال فترة زمنية، تُظهر الميزانية العمومية الوضع المالي للشركة في لحظة معينة، مثل نهاية ربع سنوي أو سنة مالية. وهي توضح ما تملكه الشركة وما عليها من التزامات ضمن فئات رئيسية: الأصول، الالتزامات، وحقوق المساهمين.

تُرتب الأصول حسب مدى سهولة تحويلها إلى نقد، بدءًا من الأكثر سيولة مثل النقد وما يعادله. وبالمثل، تُصنف الالتزامات بدءًا من الالتزامات قصيرة الأجل ثم الديون والالتزامات طويلة الأجل.

The working capital figure directly reflects the company’s ability to cover its short-term obligations. Let’s now move on to the formula used to calculate working capital.

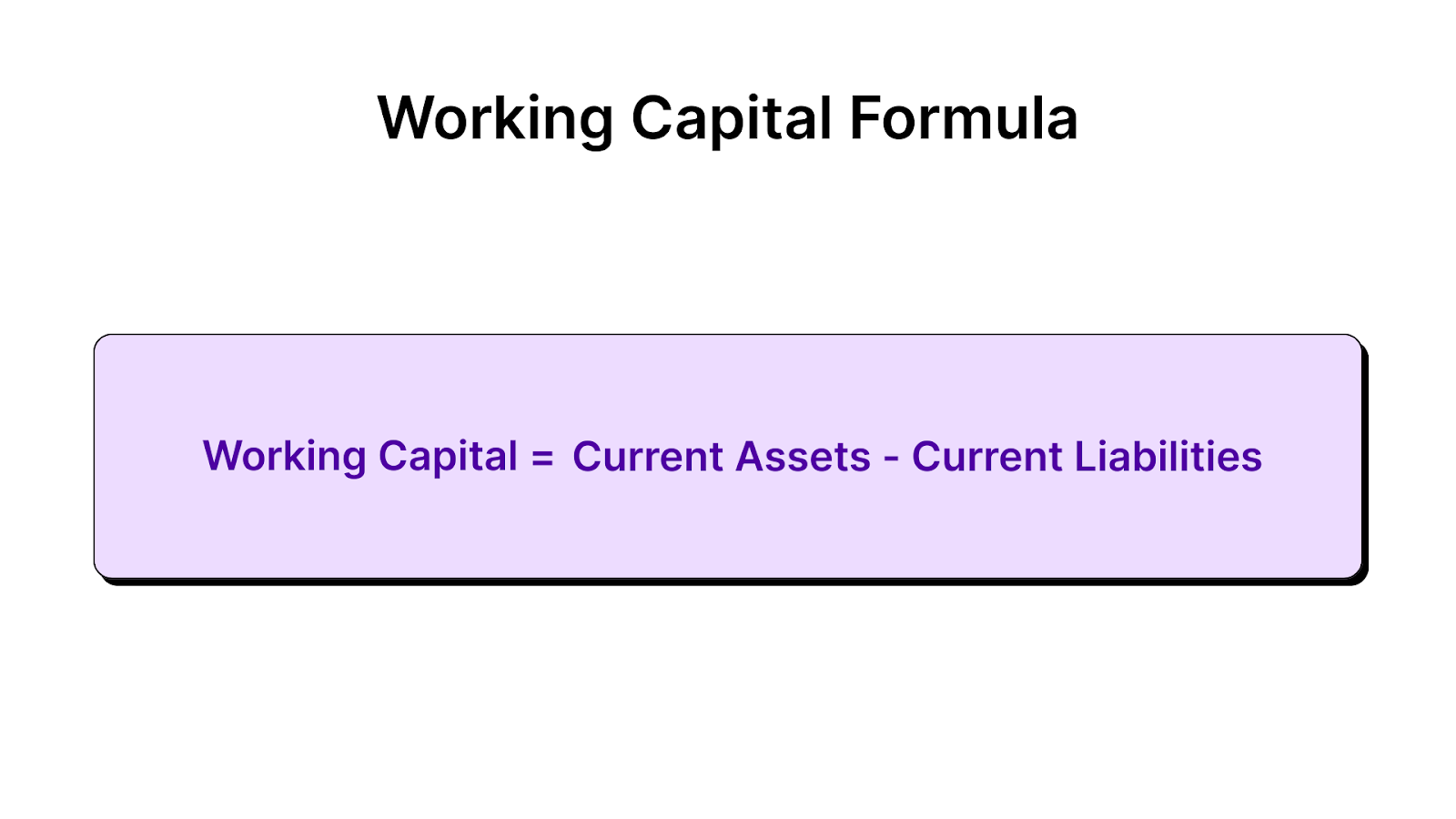

صيغة رأس المال العامل

صيغة حساب رأس المال العامل بسيطة:

رأس المال العامل = الأصول المتداولة − الالتزامات المتداولة

حيث:

الأصول المتداولة: هي الأصول التي يُتوقع تحويلها إلى نقد أو استخدامها خلال سنة واحدة (مثل النقد، الحسابات المدينة، والمخزون).

الالتزامات المتداولة: هي الالتزامات المستحقة خلال سنة واحدة (مثل الحسابات الدائنة، القروض قصيرة الأجل، والأجور).

رأس المال العامل الإيجابي مقابل السلبي

يمكن أن يكون رأس المال العامل إيجابيًا أو سلبيًا:

رأس مال عامل إيجابي: يدل على أن الشركة تمتلك أصولًا كافية لتغطية التزاماتها قصيرة الأجل، ويُعد عادةً مؤشرًا على صحة مالية جيدة.

رأس مال عامل سلبي: يشير إلى أن الشركة قد لا تمتلك أصولًا كافية لتغطية التزاماتها قصيرة الأجل، مما قد يدل على مشكلات في السيولة.

مثال

دعونا نلقي نظرة على مثال بسيط لفهم كيفية عمل رأس المال العامل عمليًا:

مثال على الميزانية العمومية لشركة XYZ Ltd. كما في 31 مارس 2025

Assets and Liabilities

Category

Amount (SAR)

Current Assets

Cash and Cash Equivalents

50,000

Accounts Receivable

30,000

Inventory

40,000

Total Current Assets

120,000

Current Liabilities

Accounts Payable

20,000

Short-term Loans

10,000

Accrued Expenses

5,000

Total Current Liabilities

35,000

Non-Current Assets

Property, Plant, and Equipment

200,000

Intangible Assets

30,000

Total Non-Current Assets

230,000

Non-Current Liabilities

Long-Term Debt

100,000

Total Liabilities

135,000

Total Assets

350,000

Equity

Shareholder’s Equity

215,000

Total Equity

215,000

نعلم الآن أن: رأس المال العامل = الأصول المتداولة − الالتزامات المتداولة

في هذه الحالة: رأس المال العامل = 120,000 ريال سعودي (الأصول المتداولة) − 35,000 ريال سعودي (الالتزامات المتداولة) رأس المال العامل = 85,000 ريال سعودي

التفسير: في هذا المثال، تمتلك شركة XYZ Ltd. رأس مال عامل قدره 85,000 ريال سعودي، مما يشير إلى أن الشركة لديها أصول كافية على المدى القصير لتغطية التزاماتها الحالية والحفاظ على سير العمليات بسلاسة.

يشير رأس المال العامل الإيجابي إلى أن الشركة في وضع مالي جيد يمكّنها من الوفاء بالتزاماتها قصيرة الأجل، كما يتيح لها فرصة استثمار الفائض في العمليات التشغيلية أو فرص النمو المستقبلية.

الآن بعد أن فهمنا كيفية حساب رأس المال العامل ودلالاته، دعنا نلقي نظرة على مكوناته بمزيد من التفصيل.

مكونات رأس المال العامل

يتأثر رأس المال العامل بعنصرين رئيسيين: الأصول المتداولة والالتزامات المتداولة. ويُعد إدارة هذه المكونات بشكل صحيح أمرًا ضروريًا للشركات للحفاظ على السيولة والاستقرار المالي.

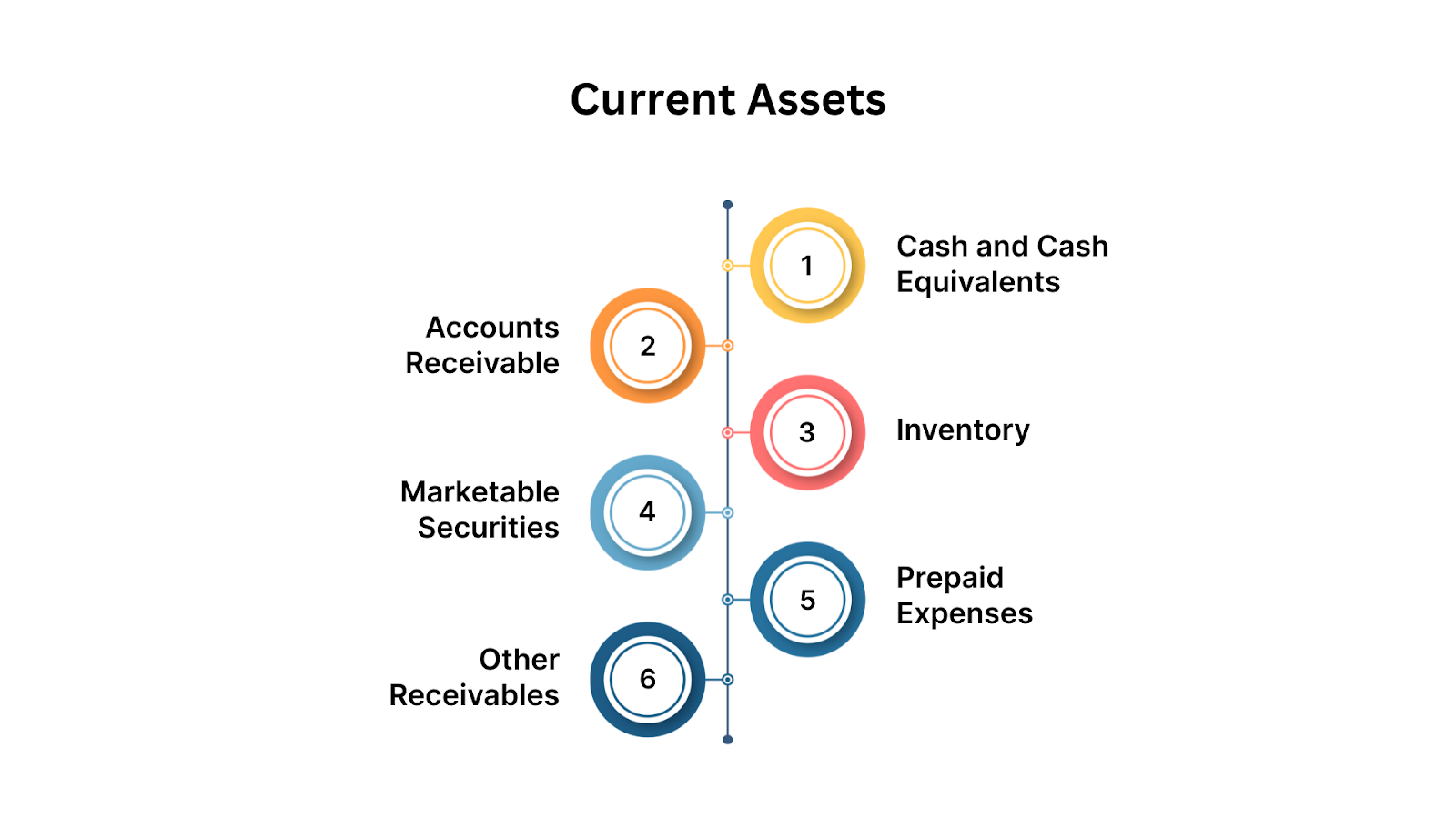

الأصول المتداولة

النقد وما في حكمه: يشمل الأموال المتاحة فورًا لتلبية الاحتياجات التشغيلية المباشرة، مثل الأموال في الحسابات البنكية والشيكات غير المودعة من العملاء.

الحسابات المدينة: هي المبالغ المستحقة على العملاء نتيجة مبيعات تمت بالآجل، وقد يتم تخفيضها بمخصصات الديون المشكوك في تحصيلها.

المخزون: يشمل السلع والمواد الخام التي يتم الاحتفاظ بها للبيع أو التي تكون قيد الإنتاج.

الأوراق المالية القابلة للتداول: استثمارات قصيرة الأجل يمكن تحويلها إلى نقد خلال سنة واحدة، مثل صناديق سوق المال أو أذون الخزانة الأمريكية.

المصروفات المدفوعة مقدمًا: هي مصاريف يتم دفعها مسبقًا، مثل أقساط التأمين، ويتم الاعتراف بها تدريجيًا مع مرور الوقت.

ذمم مدينة أخرى: تشمل عناصر مثل استرداد الضرائب، والسلف النقدية للموظفين، والمبالغ الأخرى المستحقة للشركة.

الالتزامات المتداولة

الحسابات الدائنة: هي المبالغ المستحقة للموردين مقابل سلع أو خدمات تم استلامها ولكن لم يتم سداد قيمتها بعد.

الديون قصيرة الأجل: تشمل القروض أو الائتمان الذي يجب سداده خلال سنة واحدة، بما في ذلك الجزء المستحق خلال السنة من الديون طويلة الأجل.

المصروفات المستحقة: هي المصروفات التي تم تكبدها ولكن لم يتم دفعها بعد، مثل الأجور والضرائب وفواتير الخدمات.

الإيرادات المؤجلة: هي مدفوعات مقدمة من العملاء مقابل سلع أو خدمات لم يتم تقديمها بعد، وسيتم الاعتراف بها كإيرادات في الفترات المستقبلية.

التزامات متداولة أخرى: تشمل الضرائب المستحقة، والفوائد المستحقة، وأي التزامات قصيرة الأجل أخرى يجب سدادها خلال السنة.

ومن خلال الإدارة الدقيقة لكل من الأصول المتداولة والالتزامات المتداولة، يمكن للشركات تحسين رأس المال العامل لديها، مما يضمن توفر السيولة اللازمة للعمليات اليومية والنمو على المدى الطويل. والآن دعنا ننتقل إلى بعض قيود رأس المال العامل.

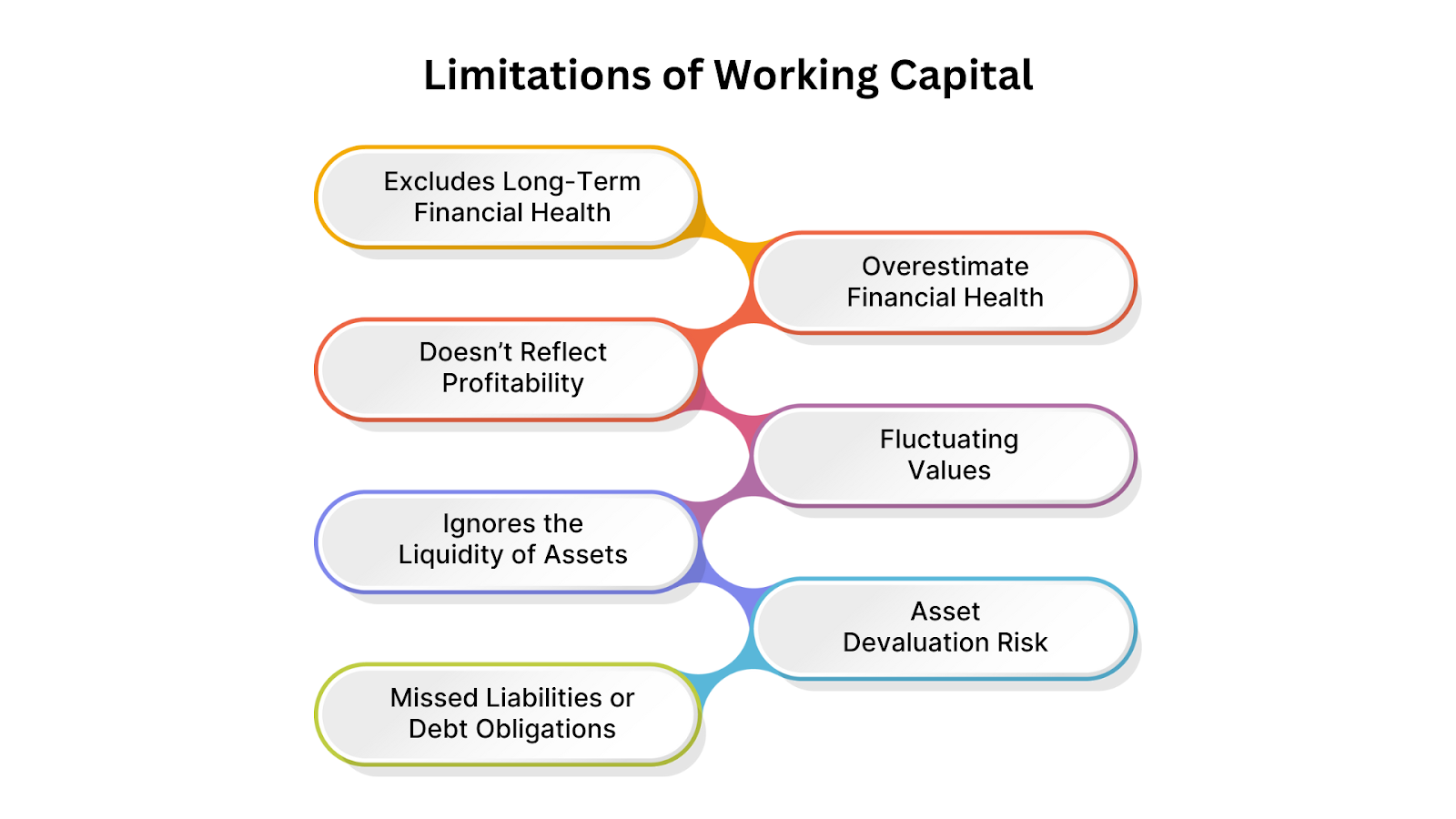

على الرغم من أن رأس المال العامل يُعد مؤشرًا ماليًا مهمًا، إلا أنه يمتلك بعض القيود التي يجب الانتباه إليها. فقد يشير ارتفاع رأس المال العامل إلى عدم كفاءة في استخدام الأصول، بينما قد يدل انخفاضه على وجود مشكلات في السيولة. وفيما يلي أبرز هذه القيود:

لا يعكس الصحة المالية طويلة الأجل: يركز رأس المال العامل على الأصول والالتزامات قصيرة الأجل فقط، ولا يأخذ في الاعتبار الديون أو الأصول طويلة الأجل التي قد تؤثر بشكل كبير على الاستقرار المالي العام.

قد يبالغ في تقدير الوضع المالي: قد يبدو ارتفاع رأس المال العامل مؤشرًا إيجابيًا، لكنه قد يعكس سوء استخدام الموارد، مثل تراكم المخزون أو تأخر تحصيل الحسابات المدينة، مما يقلل من السيولة الفعلية.

لا يعكس الربحية: لا يوجد ارتباط مباشر بين رأس المال العامل والربحية، فقد تمتلك الشركة رأس مال عامل إيجابي لكنها تعاني من ضعف هوامش الربح أو سوء إدارة التدفقات النقدية.

تقلب القيم باستمرار: يتغير رأس المال العامل بشكل يومي مع حركة العمليات التشغيلية، مما يجعل الأرقام المستخدمة في حسابه غير دقيقة دائمًا عند التقييم في وقت لاحق، خاصة في القطاعات الموسمية أو سريعة التغير.

لا يأخذ في الاعتبار سيولة الأصول: ليست كل الأصول ضمن رأس المال العامل سهلة التحويل إلى نقد، مثل المخزون الراكد أو الحسابات المدينة المتأخرة، مما قد يؤدي إلى مشاكل سيولة رغم ارتفاع الرقم الإجمالي.

خطر انخفاض قيمة الأصول: قد تنخفض قيمة الأصول مثل المخزون أو الذمم المدينة بسبب تقادم المنتجات أو تعثر العملاء، مما يؤدي إلى تضخيم قيمة رأس المال العامل.

إغفال بعض الالتزامات: قد لا تعكس الحسابات جميع الالتزامات الفعلية في حال وجود مصروفات غير مسجلة أو ديون غير موثقة، مما يؤدي إلى تشويه دقة الحساب.

ورغم هذه القيود، يظل رأس المال العامل مؤشرًا أساسيًا لفهم السيولة التشغيلية للشركات. والآن، دعنا ننتقل إلى كيفية زيادة رأس المال العامل في الأعمال.

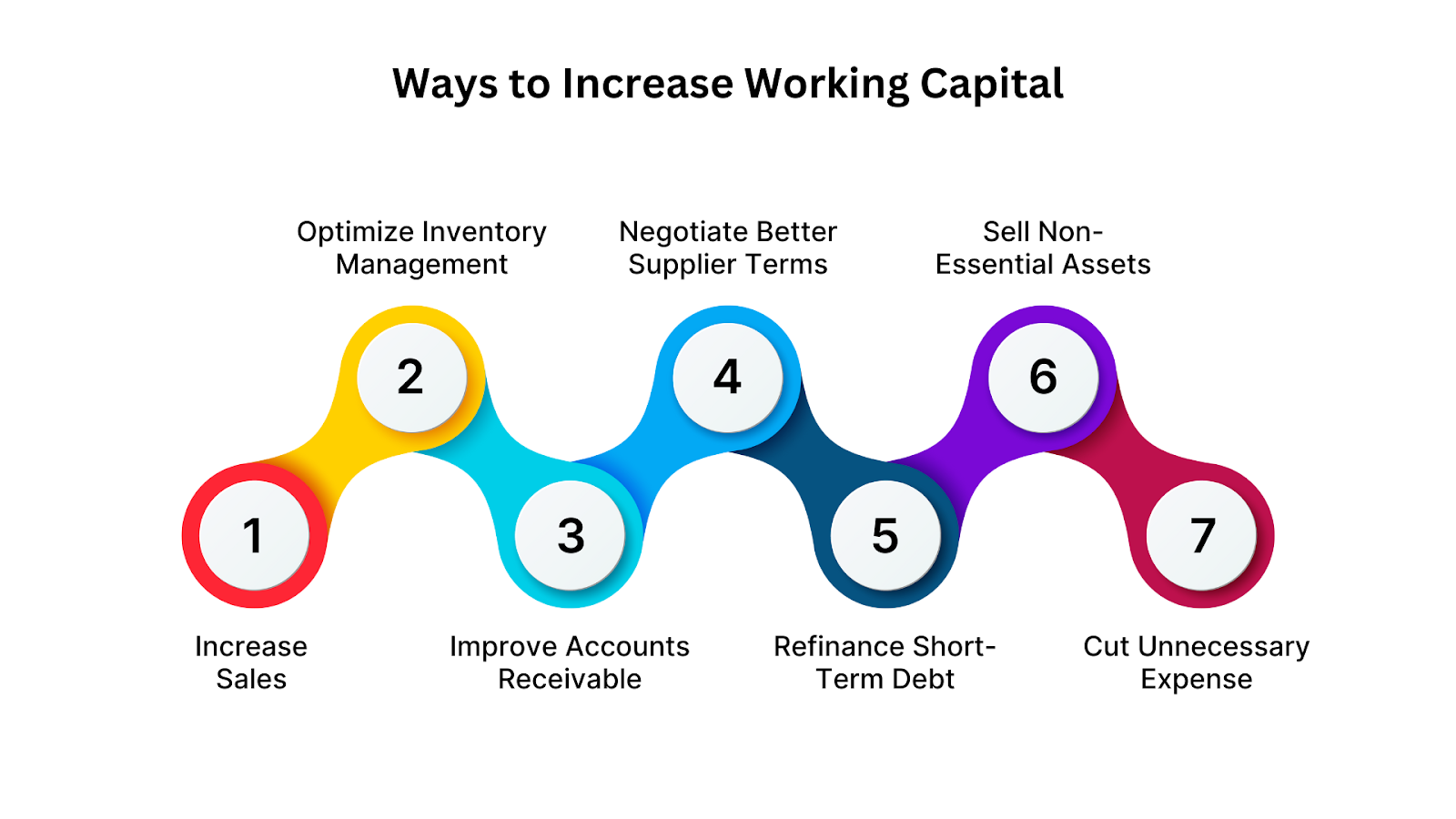

طرق زيادة رأس المال العامل

طرق زيادة رأس المال العامل

يُعد تعزيز رأس المال العامل خطوة مهمة للشركات التي تسعى لتحسين وضعها المالي واغتنام فرص النمو. فمن خلال زيادة توفر النقد، يمكن ضمان استمرارية العمليات اليومية والاستعداد بشكل أفضل للتحديات غير المتوقعة. فيما يلي أبرز الاستراتيجيات الفعّالة:

زيادة المبيعات: يُعد نمو الإيرادات من أبسط الطرق لرفع رأس المال العامل، حيث يؤدي ارتفاع المبيعات إلى زيادة التدفقات النقدية وتحسين السيولة.

تحسين إدارة المخزون: يساعد تقليل المخزون الزائد على تحرير النقد المجمد، ويمكن تحقيق ذلك عبر اعتماد نظام المخزون الفوري أو التخلص من البضائع بطيئة الحركة.

تحسين الحسابات المدينة: تسريع تحصيل الفواتير المستحقة يقلل دورة التحويل النقدي. ويمكن تحفيز العملاء عبر تشديد سياسات الائتمان أو تقديم خصومات للسداد المبكر.

التفاوض على شروط أفضل مع الموردين: تمديد فترات السداد يسمح بالاحتفاظ بالنقد لفترة أطول، مما يعزز السيولة دون الإضرار بالعلاقات التجارية.

إعادة تمويل الديون قصيرة الأجل: تحويل القروض قصيرة الأجل إلى ديون طويلة الأجل يقلل الضغط المالي الفوري ويوفر مرونة أكبر في إدارة العمليات.

بيع الأصول غير الأساسية: في حال الحاجة إلى سيولة سريعة، يمكن بيع الأصول غير المرتبطة بالنشاط الأساسي للشركة.

خفض المصروفات غير الضرورية: يساعد تقليل التكاليف التشغيلية غير الأساسية على تقليل الالتزامات الحالية وتحسين التدفقات النقدية، مما يضمن استخدام كل ريال بكفاءة أعلى.

ومن خلال تطبيق هذه الاستراتيجيات، تستطيع الشركات تعزيز رأس المال العامل لديها وضمان توفر الموارد اللازمة لاستمرار العمليات وتمويل فرص النمو المستقبلية.

يتطلب تحسين رأس المال العامل أكثر من حلول سريعة؛ فهو يحتاج إلى وضوح في الرؤية، وتحكم دقيق، وإدارة مالية ذكية. ويوفر نظام HAL ERP الأدوات اللازمة لتحقيق استقرار مالي مستدام.

يدعم HAL ERP الإدارة المالية الفعّالة

يوفر نظام HAL ERP للشركات الأدوات اللازمة لتحسين عمليات الإدارة المالية، بما في ذلك تحسين رأس المال العامل. وقبل استعراض مزاياه، دعنا نلقي نظرة على دراسة حالة واقعية.

دراسة حالة: مجموعة الحميضي

قامت مجموعة الحميضي، إحدى أبرز سلاسل التجزئة الفاخرة في المملكة العربية السعودية والتي تمتلك أكثر من 80 فرعًا على مستوى المملكة، بتحديث عملياتها المالية والتشغيلية من خلال التحول إلى نظام HAL ERP. وكانت النتائج مميزة:

تحقيق أكثر من 70 مليون ريال سعودي من الوفورات التشغيلية من خلال الأتمتة وتكامل الأنظمة.

زيادة العائد على الاستثمار بنسبة 61% بفضل التقارير الفورية، وإدارة المخزون الدقيقة، والتحليلات المتقدمة.

تبسيط عمليات المبيعات والمخزون مع إمكانية الوصول إليها من أي مكان عبر تطبيقات الجوال.

تعزيز الحوكمة والرقابة على التسعير والخصومات عبر فروع التجزئة المختلفة.

تسريع عمليات إغلاق نهاية الشهر وتحسين سرعة ودقة اتخاذ القرار المبني على البيانات.

تعكس هذه التحولات الأثر الملموس الذي يقدمه نظام HAL ERP، من خلال دمج الأتمتة، والامتثال، والرؤى الفورية لتسريع نمو الأعمال.

كيفية إدارة الأمور المالية بسهولة مع HAL ERP

بفضل الميزات المصممة لأتمتة المهام الأساسية وتعزيز الكفاءة، يمكن للشركات تحسين التدفقات النقدية، وتقليل الأخطاء، والحفاظ على الاستقرار المالي. إليك كيف يساعد HAL ERP الشركات على إدارة أمورها المالية بشكل أكثر فعالية:

إدخالات اليومية المحاسبية الآلية: يقوم HAL ERP بأتمتة القيود المحاسبية، مما يضمن الدقة ويقلل الوقت المستغرق في الإدخال اليدوي، ويساعد على الحفاظ على سجلات مالية محدثة ودقيقة لرأس المال العامل.

تسوية بنكية فعّالة: يسهّل مطابقة السجلات البنكية مع البيانات المالية تلقائيًا، مما يوفر الوقت ويقلل الفروقات بين كشوفات الحسابات والسجلات الداخلية.

حل قائم على السحابة: يتيح النظام الوصول إلى البيانات المالية من أي مكان، مما يوفر مرونة عالية وقدرة على اتخاذ القرار في أي وقت ومن أي موقع.

تقارير شاملة: إمكانية إنشاء تقارير مالية تفصيلية بسهولة لمتابعة رأس المال العامل، وتحليل التغيرات، واتخاذ قرارات مالية مدروسة.

معالجة العمليات دفعة واحدة: تنفيذ عدة عمليات مثل المصروفات أو القيود أو التحويلات دفعة واحدة، مما يزيد الإنتاجية ويقلل الوقت المستغرق.

أمان وصلاحيات وصول متقدمة: يوفر النظام إدارة آمنة للبيانات مع تحكم دقيق في صلاحيات المستخدمين لضمان حماية المعلومات المالية.

الامتثال المحلي: يتوافق HAL ERP مع متطلبات SAMA وهيئة الزكاة والضريبة والجمارك (ZATCA) وضريبة القيمة المضافة في السعودية، مما يضمن التزامًا قانونيًا سلسًا.

حلول مناسبة للميزانية: يقدم HAL ERP حلولًا بأسعار مناسبة للشركات بمختلف أحجامها، مع خطط تبدأ من 1,999 ريال سعودي سنويًا.

لا تستفيد الشركات التي تستخدم HAL ERP من تبسيط العمليات فحسب، بل تشهد أيضًا تحسنًا في إدارة التدفقات النقدية والحصول على رؤى محدثة حول صحتها المالية. اكتشف كيف ساعد HAL ERP شركات أخرى من خلال استعراض قصص النجاح الخاصة بنا.

الخاتمة

يلعب رأس المال العامل دورًا محوريًا في ضمان المرونة المالية والنجاح التشغيلي لأي شركة. فمن خلاله تستطيع الشركات الحفاظ على عملياتها اليومية واغتنام فرص النمو الجديدة، مما يجعله عنصرًا أساسيًا للاستقرار وقابلية التوسع.

إن امتلاك مستوى صحي من رأس المال العامل يساعد الشركات على فهم مكوناته، وحسابه بدقة، وتطبيق استراتيجيات فعّالة لتحسينه، وبالتالي التحكم بشكل أفضل في صحتها المالية قصيرة الأجل.

ولا يقتصر تحسين رأس المال العامل على تطبيق أفضل الممارسات فقط، بل يتطلب أنظمة فعّالة لمتابعة البيانات وإدارتها واتخاذ القرارات في الوقت الفعلي. وهنا يبرز دور HAL ERP.

حسّن إدارة رأس المال العامل لديك مع HAL ERP. بسّط عملياتك المالية وارتقِ بأداء أعمالك اليوم. احجز عرضًا توضيحيًا الآن!