Property Management Chart of Accounts: Structure, Setup & Best Practices

Published By

Umar Shariff

Finance - General Accounting

Apr 3, 2026

In 2026, Saudi Arabia’s real estate market sits at an estimated USD 72.84 billion and is projected to continue growing strongly in the coming years. This rapid expansion is driven by urbanization, diversified investment flows, and ongoing demand for residential and commercial properties.

But with growth comes complexity. Managing a property portfolio means not just collecting rent and paying bills, but also tracking asset performance, owner distributions, trust liabilities, and VAT compliance across multiple entities. Without a clear financial framework, reporting becomes inconsistent, risk rises, and strategic decisions are clouded.

In this blog you’ll learn what property management chart of accounts are, why it matters, how to structure core accounts for property businesses, practical implementation steps you can follow, and how automation can simplify the entire process.

Key Takeaways

A property management chart of accounts creates financial structure by clearly separating operational income, trust funds, owner obligations, and compliance balances.

Proper account segmentation enables accurate property-level profitability reporting without relying on manual spreadsheets or post-period reclassification.

Trust accounting, VAT control, and owner distributions require dedicated accounts to prevent misstatement and regulatory risk.

Implementation discipline, including system mapping, migration cleanup, and testing, determines whether the COA performs reliably in real operations.

ERP automation strengthens consistency by embedding posting logic, VAT alignment, and reconciliation controls directly into daily workflows.

What is a Property Management Chart of Accounts?

A property management chart of accounts (COA) is the structured list of every financial account a property business uses to record transactions. It groups accounts into balance sheet and profit-and-loss categories, assets, liabilities, equity, revenue, and expenses, and provides the numbering and naming conventions that let you post, aggregate, and report consistently across properties and entities.

For property managers and landlords, the COA is the base of reporting: it turns lease billing, service charges, repairs, owner distributions, and trust activity into usable P&Ls, owner statements, VAT returns, and audit trails.

A well-designed COA also supports dimensional tagging (property, building, unit) so a single ledger can produce property-level profitability without manual spreadsheets.

Why is a Chart of Accounts Important?

A good COA directly affects decision-making, compliance, and operational control. Key reasons it matters for property businesses:

Enables accurate property P&Ls: Proper account granularity and property tags let you see income and expense by building or unit, not just at the corporate level.

Supports owner and trust accounting: Segregated accounts for owner funds, security deposits, and trust liabilities prevent fund commingling and simplify owner statements.

Simplifies VAT and e-invoicing compliance: COA alignment with VAT collectible/recoverable accounts and invoice traceability makes ZATCA reporting and VAT returns cleaner.

Speeds month-end close and reporting: Consistent account structures reduce reconciliation work and eliminate ad-hoc reclassification during close.

Supports growth and consolidation: A standardized numbering and tagging scheme scales across portfolios and eases multi-entity consolidations.

For mid-sized property businesses in Saudi Arabia, a chart of accounts acts as a decision framework. When it is inconsistent, profitability across properties becomes unclear, costs are hard to track, and reports arrive too late to act on. A well-structured COA brings clarity across units and entities, giving founders and finance leaders a reliable view of performance so they can make faster, more confident decisions.

Once the importance is clear, the practical question becomes structural. What does a properly designed property management chart of accounts actually look like in practice?

That structure begins with defining the core account groups.

How to Structure the Core Accounts in a Property Management Chart of Accounts

A property management chart of accounts should mirror how money actually moves through a property portfolio. Rent is collected, deposits are held, vendors are paid, owners are distributed, VAT is calculated, and capital improvements are recorded. If the account structure does not clearly separate these flows, reporting becomes unreliable and compliance risk increases.

Let's breaks down the essential account groups that form a stable property management chart of accounts:

1. Asset Accounts

Asset accounts represent what the property business controls or expects to receive. In property management, clarity in asset classification is critical because operating funds and client-related funds must never be mixed.

Defined asset components typically include:

Operating bank accounts: Cash used for day-to-day property expenses such as utilities, maintenance, and payroll.

Trust or escrow bank accounts: Separate accounts holding tenant deposits or owner funds to prevent commingling.

Tenant receivables: Outstanding rent, service charges, or other billings due from tenants.

Prepaid expenses: Payments made in advance, such as insurance or annual service contracts.

Fixed assets by property: Capital improvements, equipment, or infrastructure tied to specific properties.

Accumulated depreciation: Systematic reduction in asset value over time.

VAT recoverable (Input VAT): Tax paid on purchases that can be reclaimed under VAT regulations.

Proper asset separation improves cash visibility and simplifies reconciliation.

Liabilities represent obligations owed to third parties, tenants, or property owners. In property management, many liabilities relate to funds held on behalf of others rather than traditional business debt.

Key liability classifications include:

Accounts payable: Approved but unpaid supplier invoices.

Tenant security deposits: Funds collected from tenants that must remain classified as liabilities until refunded or applied.

Deferred rental income: Advance rent received but not yet earned.

Owner payable balances: Net rental income due to property owners after expenses and management fees.

VAT payable (Output VAT): Tax collected on rental or service income that must be remitted.

Loans and mortgage balances: Financing obligations tied to property acquisitions.

Clear liability categorization prevents revenue misstatement and strengthens compliance control.

3. Equity Accounts

Equity accounts reflect the ownership structure of the property entity or management company. While these are less operational, they are essential for accurate financial reporting and consolidation.

Standard equity elements include:

Paid-in capital: Investment contributions from owners or shareholders.

Retained earnings: Accumulated profits from prior years.

Current year earnings: Net income generated during the current reporting period.

For multi-entity portfolios, equity tracking supports consolidation and group-level reporting accuracy.

4. Revenue Accounts

Revenue accounts must provide visibility into how income is generated across properties. A single “Rental Income” account is rarely sufficient for performance analysis.

Defined revenue categories should include:

Base rental income: Core lease payments from residential or commercial tenants.

Service charge or CAM recoveries: Reimbursements for common area maintenance costs.

Parking or ancillary rental income: Income from additional leased spaces or facilities.

Late payment penalties and fees: Charges applied for overdue rent.

Other property-related income: Advertising space, storage, or amenity-based earnings.

Segmentation allows property-level profitability analysis and supports VAT treatment where applicable.

5. Expense Accounts

Expense structure determines how clearly management can understand property performance. Poor expense grouping hides cost drivers and reduces margin transparency.

Well-defined expense accounts typically include:

Repairs and maintenance: Categorized by type, such as HVAC, plumbing, electrical, or general repairs.

Utilities: Electricity, water, waste management, and related services.

Property management fees: Fees charged to owners for managing the property.

Insurance and municipal charges: Regulatory or coverage-related expenses.

Marketing and leasing costs: Advertising, brokerage, and tenant acquisition expenses.

Cleaning and security services: Operational building costs.

Depreciation expense: Allocation of capital asset costs over useful life.

Detailed expense classification improves budgeting accuracy and cost control.

6. Compliance and Control Accounts

Property management businesses operating in Saudi Arabia require dedicated accounts to manage regulatory obligations effectively.

These typically include:

VAT recoverable and VAT payable control accounts: Separate tracking of input and output VAT for reconciliation.

ZATCA-related adjustment accounts: For compliance corrections or penalties if applicable.

Trust clearing accounts: Temporary holding accounts to manage owner or tenant fund transfers.

Intercompany balances: Required for businesses managing properties under multiple legal entities.

These control accounts reduce reporting risk and simplify regulatory filings.

A properly structured property management chart of accounts clearly separates operational activity, trust balances, owner obligations, and compliance accounts.

The real difference shows up in how the chart is implemented inside your systems and workflows.

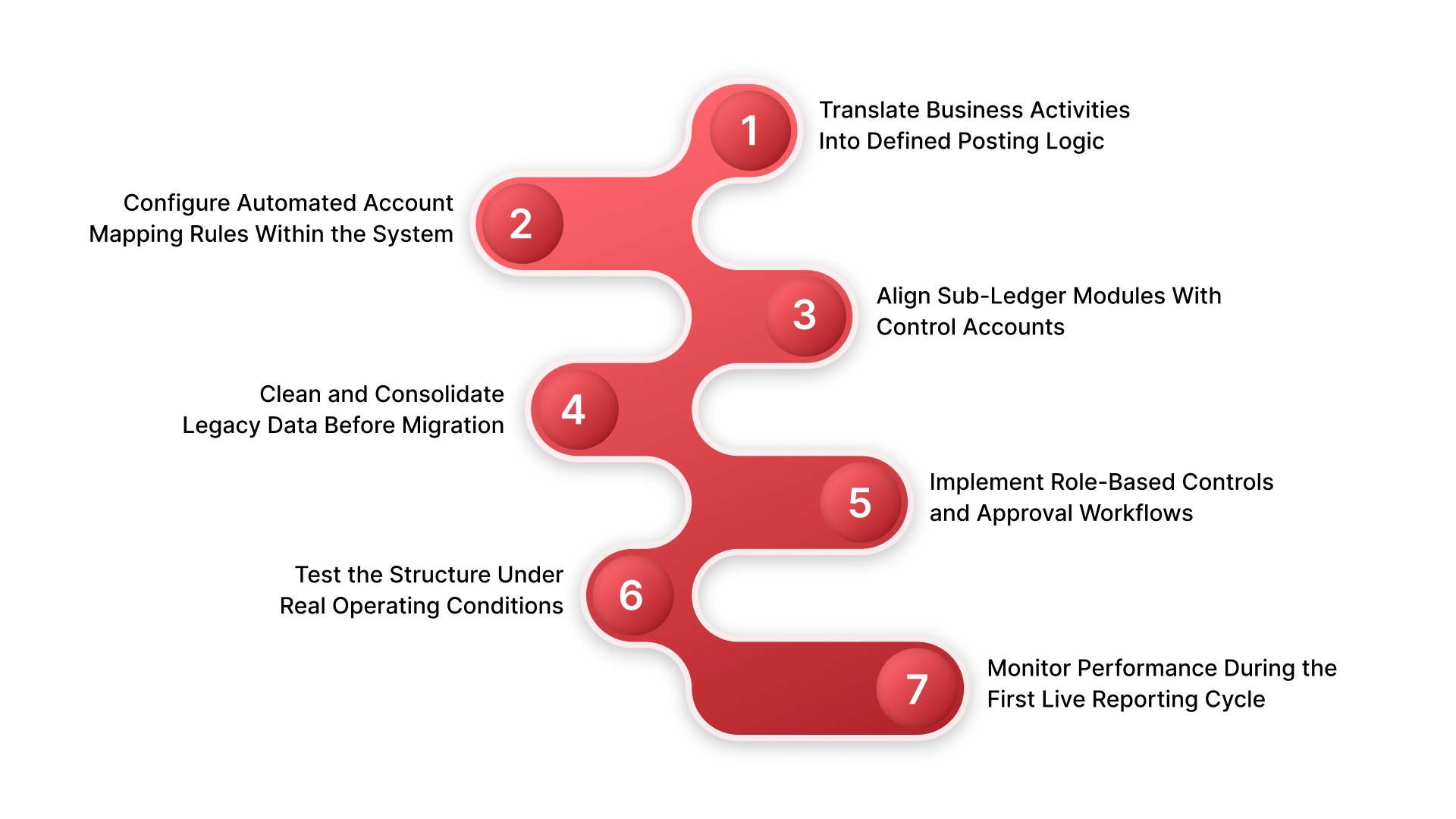

Practical Implementation Steps to Build a Property Management Chart of Accounts

Designing the account categories defines structure. Implementation defines performance. A property management chart of accounts only becomes effective when it is embedded into real transaction flows, system configurations, and internal controls:

1. Translate Business Activities Into Defined Posting Logic

Every property business runs on recurring financial events: rent billing, maintenance work orders, service charge allocations, deposits, and owner settlements. If those events are not mapped to specific ledger destinations with clarity, posting inconsistencies accumulate over time.

Before configuration begins, document how money flows through your business.

Map lease lifecycle events to revenue accounts: Identify how new leases, renewals, rent escalations, and early terminations are recorded. Define which revenue accounts capture base rent versus recoveries or penalty fees.

Define deposit handling logic from collection to refund: Clarify how tenant security deposits are recorded at receipt, where they are held, and how partial deductions or full refunds are posted. The lifecycle of a deposit should never touch revenue accounts.

Separate capital expenditure from routine maintenance at source: Establish rules that distinguish between asset capitalization and expense recognition. Without this clarity, depreciation schedules and expense reporting become distorted.

Outline owner distribution mechanics: Define how net income is calculated, which expenses are deducted before distribution, and how management fees are applied.

Clear posting logic ensures similar transactions receive identical treatment across reporting periods.

2. Configure Automated Account Mapping Rules Within the System

Once logic is documented, automation should enforce it. Manual selection of account codes during posting introduces inconsistency and increases reconciliation workload.

System configuration should formalize financial treatment.

Set revenue defaults within lease templates: Configure billing modules so each charge type automatically maps to the correct revenue account. For example, base rent, parking income, and service charges should never rely on manual coding.

Assign vendor categories to expense accounts: Link supplier classifications, such as electrical contractors or cleaning services, to predefined expense accounts.

Define allocation rules for shared property costs: If utilities or security expenses are shared across multiple units, configure allocation percentages in advance. This reduces recurring manual adjustments.

Automate depreciation and amortization schedules: Tie asset classes to defined useful lives and expense accounts. Automation ensures depreciation entries post consistently each period.

Property operations typically rely on multiple modules: leasing, procurement, asset management, and sometimes facility management systems. Each module feeds financial data into the general ledger.

Alignment between modules and control accounts must be validated early.

Reconcile tenant receivable modules to AR control accounts: The total outstanding tenant balance should always match the accounts receivable control balance in the ledger. Any difference indicates mapping or posting errors.

Confirm vendor ledger totals match accounts payable balances: Supplier sub-ledger balances must tie to the AP control account to ensure payable reporting remains accurate.

Integrate asset registers with depreciation expense accounts: Fixed asset additions, disposals, and depreciation entries should post automatically without manual reclassification.

Validate VAT treatment between invoicing and tax control accounts: Ensure VAT generated through billing modules posts directly to designated VAT payable accounts and that input VAT from vendor invoices maps correctly to recoverable accounts.

4. Clean and Consolidate Legacy Data Before Migration

Migration is where structural clarity can break down. If old account codes are duplicated, inconsistently named, or poorly grouped, transferring them directly into the new structure will carry forward historical confusion.

Preparation is critical.

Eliminate redundant or unused accounts: Remove obsolete codes that no longer reflect operational needs.

Standardize naming conventions: Ensure consistent terminology across accounts. For example, avoid mixing “Repairs,” “Maintenance,” and “R&M” across different codes.

Map legacy codes to the new structure with documented logic: Create a migration mapping sheet that shows exactly how old accounts transition into new ones.

Reconcile opening balances before go-live: Validate that transferred balances tie to bank statements, tenant aging reports, and vendor ledgers. Errors at this stage cascade into future reporting cycles.

Migration discipline protects the integrity of the new chart of accounts.

5. Implement Role-Based Controls and Approval Workflows

Financial structure must be supported by governance controls. Without role clarity, even a well-designed chart of accounts can be misused.

Define authority and accountability clearly.

Establish posting permissions by function: Limit who can create, edit, or post transactions to reduce accidental misclassification.

Require approval for high-value or sensitive entries: Expense thresholds and capital expenditures should require documented approval before posting.

Mandate documentation for manual journal entries: Any non-automated entry should include a clear explanation and supporting evidence.

Separate transaction entry from financial review: Implement segregation between those who record transactions and those who approve financial reports.

Governance strengthens reliability and audit defensibility.

6. Test the Structure Under Real Operating Conditions

Before full reliance, validate the structure through controlled testing. Theory must match practice.

Simulate end-to-end financial activity.

Run a full lease billing cycle: Confirm revenue, VAT, and receivable balances post correctly.

Process vendor invoices across categories: Verify expense mapping and VAT input treatment.

Execute deposit receipt and refund transactions: Ensure liability balances adjust correctly without affecting income.

Generate property-level P&Ls and owner summaries: Confirm reporting outputs align with management expectations.

Produce a VAT summary for the test period: Validate that tax balances reconcile to invoicing and expense totals.

Testing identifies gaps before they become systemic.

7. Monitor Performance During the First Live Reporting Cycle

Implementation is not complete at activation. The first reporting cycle reveals whether the structure performs under real operational volume.

During the initial month:

Track the number of manual journal corrections

Monitor reconciliation exceptions

Review property-level margin consistency

Confirm VAT balances reconcile without reclassification

Early observation allows refinement before inefficiencies become embedded in routine processes.

As portfolios grow, transaction volumes increase, and compliance demands tighten, system enforcement becomes critical.

This is where ERP automation shifts the conversation from structure to performance.

How HAL ERP Automates and Controls Property Management Charts of Accounts?

A property management chart of accounts only works when it is embedded into daily operations. If leasing, billing, vendor management, and VAT reporting sit in separate tools, finance ends up reconciling instead of analyzing.

HAL ERP connects property operations directly to the general ledger so your chart of accounts is enforced automatically, consistently, and in real time across your portfolio.

Here’s how HAL turns structure into controlled automation:

Real-Time Revenue Mapping from Lease to Ledger: Rental income, service charges, late fees, and other property revenues post automatically into predefined revenue accounts as soon as billing is generated. This eliminates manual coding errors and ensures consistent classification across properties.

Automated Expense Categorization at Source: Vendor categories and procurement workflows are linked to structured expense accounts. When invoices are recorded, they map directly to the correct ledger accounts.

Integrated VAT and ZATCA Alignment: Output VAT from tenant billing and input VAT from supplier invoices are automatically directed to designated VAT control accounts. With built-in e-invoicing support and Fatoora portal readiness, HAL keeps property accounting aligned with ZATCA compliance requirements.

Deposit and Liability Control Automation: Security deposits, retention amounts, and other tenant liabilities are recorded in structured liability accounts, preventing accidental revenue misstatement and protecting trust accounting integrity.

Asset Capitalization and Depreciation Scheduling: Capital expenditures linked to property improvements feed directly into fixed asset registers. Depreciation entries are generated automatically based on configured useful lives.

Property-Level Reporting Without COA Duplication: Instead of creating separate account codes for each property, HAL uses structured tagging and segmentation. This keeps the chart clean while enabling detailed P&L reporting by property, building, or portfolio.

AI-Assisted Bank Reconciliation: Bank transactions are matched automatically against ledger entries, highlighting only exceptions for review. This reduces reconciliation time and strengthens cash accuracy.

Multi-Entity and Intercompany Support: For property groups operating under multiple legal entities, HAL synchronizes intercompany transactions and enables consolidated reporting without manual elimination errors.

Conversational Financial Reporting via HALA: Finance leaders can request trial balances, property-level P&Ls, or VAT summaries directly through WhatsApp. Reports are generated instantly and can be filtered, customized, and shared without exporting spreadsheets.

Fast Deployment with Dedicated Transition Teams: Basic finance setup can go live within 2–4 weeks, with full property portfolio implementation typically completed in 8–12 weeks, supported by HAL’s dedicated onboarding team.

HAL ERP embeds your property management chart of accounts into operations, compliance, and reporting layers so financial accuracy is system-driven.

Conclusion

A clear COA is the difference between reactive bookkeeping and forward-looking property finance. Start by auditing your current chart for misplaced deposits, mixed accounts, and missing VAT controls. Then map core workflows into posting rules and test them in a staging environment before full migration.

If you want the technical heavy lifting done faster, HAL ERP can automate posting, VAT alignment, deposit controls, and property tagging while keeping implementation practical. Book a demo to see how your COA would look in a live property stack and to get a tailored migration checklist.

FAQs

1. How detailed should a property management chart of accounts be?

The level of detail should match your reporting needs. Too few accounts limit insight, while excessive fragmentation creates complexity. A balanced structure allows property-level analysis without overcomplicating transaction entry.

2. Can a single chart of accounts work for mixed portfolios (residential and commercial)?

Yes, but it requires careful revenue and expense segmentation. Commercial leases often include recoveries and variable charges that must be separated clearly from residential rental income.

3. When should you redesign your property management chart of accounts?

Redesign is typically needed when expanding into new property types, adding multiple entities, facing recurring reconciliation issues, or preparing for regulatory audits.

4. How does a chart of accounts impact budgeting and forecasting?

A structured COA improves forecast reliability because historical financial data is categorized consistently. This makes variance analysis and long-term planning more accurate.

5. What risks arise from an outdated or poorly structured COA?

Common risks include revenue misclassification, deposit commingling, VAT errors, inaccurate owner distributions, and prolonged month-end closing cycles.

Umar Shariff

Umar Shariff is a serial entrepreneur and CEO of HAL Simplify, celebrated for making ERP platforms seamless and intuitive for Middle Eastern organizations. With extensive experience scaling team and driving digital transformation projects in Saudi Arabia with accelerated deployment, Umar excels at operational management, team leadership, and delivering future-ready ERP systems that elevate regional business performance.

%201.webp)

%201.webp)