.jpg)

Are unpaid invoices still draining your cash flow and holding back growth?

In Saudi Arabia, SME lending has reached a record SAR 420.7 billion in mid-2025, a 37% increase from the same period last year. Liquidity is available, but only if companies manage credit and collections rigorously.

Yet, even as credit expands, many SMEs find themselves trapped under mounting bad debt caused by delayed payments, weak credit controls, or informal terms.

Left unchecked, these overdue receivables tie up working capital, raise financing costs, and threaten operational continuity.

In this guide, you will know why SMEs struggle to recover bad debt and learn 10 practical, time-tested strategies to recover outstanding payments quickly. You will also understand common mistakes to avoid so you can protect margins and restore healthy cash flow.

Small and mid-sized businesses across Saudi Arabia are operating in a high-cost, fast-moving environment where delayed payments can quickly turn into serious cash flow problems. Even profitable companies face liquidity gaps not because of poor demand, but because revenue is trapped in unpaid invoices.

Here are a few of the root causes that turn bad debt recovery into a persistent challenge:

Must Read: What is budgeting, how is it prepared, and what are its different types?

Bad debt in Saudi Arabia is rarely a single event; it’s the result of operational gaps combined with economic pressure. To reduce risk, SMEs need proactive systems, disciplined credit management, and smarter decision-making.

Are you still trying to manage collections manually, even though firms using advanced ERP tools are seeing over 60% gains in operational efficiency and faster recovery cycles?

%20(2).png)

Now, let’s discuss some proven strategies that help growing businesses recover bad debt faster and protect long-term cash flow.

Traditional collection tactics are slow, expensive, and ineffective. Bad debt recovery in 2026 demands a more mature and proactive approach than simply chasing overdue invoices. Businesses that recover debt successfully now focus on structure, data, and consistency rather than reactive firefighting.

Saudi Arabia’s SME sector is central to the country’s economic transformation. Under Vision 2030, the Kingdom aims to increase SME contribution to GDP from 30% to 35%, and with over 1.8 million SMEs operating nationwide, ensuring stable cash flow for this segment is not just smart business; it’s a national economic priority.

Below are 10 actionable bad debt recovery strategies that help Saudi businesses reduce overdue receivables, improve collection speed, and protect working capital in a volatile business environment:

Ensure your payment terms are clearly stated on all invoices, contracts, and websites. Discuss terms with customers upfront so they know their obligations, including any late payment fees or early payment incentives.

Issue invoices immediately after a sale or service completion. A systematic follow-up schedule with automated reminders ensures consistency and catches overdue accounts early, significantly increasing the likelihood of recovery.

For example, a pharmacy chain in Jeddah can send e-invoices within 24 hours of supplying medicines to clinics, followed by reminders at 7 and 14 days. If unpaid at day 30, the system automatically flags the account and pauses further credit orders. It keeps cash flow stable without manual chasing.

Use data analytics to assess customer creditworthiness before extending credit. SMEs must focus on collection efforts on accounts that represent the highest financial impact or risk of non-recovery.

Consider Reading: How to Create a Contingency Budget for Project Management?

Initiate a polite reminder process shortly after a due date (e.g., 30 days past due). Personalize communication to individual circumstances, create a human connection and make debtors more likely to engage and cooperate.

Sample Template:

Assalamu Alaikum, Mr. Ahmed,

We hope you are doing well and business is good.

This is a friendly reminder regarding Invoice #INV-2025, issued on 06 December 2025, with an outstanding amount of SAR 22,450, which is now 30 days past due.

We understand that delays can happen due to operational priorities, and we value our relationship with [Company Name]. Kindly let us know if you need a revised schedule, supporting documents, or assistance from our side.

For your convenience, here is the payment link/details:

Bank: Al Rajhi Bank

IBAN: SAxx xxxx xxxx xxxx

If the payment has already been completed, please share the confirmation so we can update our records.

We appreciate your prompt attention and look forward to continuing our successful partnership.

Jazakum Allah Khair,

Sarah Al-Humaid

Accounts Receivable

[Your Company Name]

Mobile: +111-222-3333

Acknowledge diverse financial situations by providing customized payment plans or extended timelines. This willingness to collaborate can improve cooperation and lead to successful debt resolution.

For Instance:

Offer small discounts for early settlement or reduced interest rates for those who adhere to new payment plans. Tangible benefits can motivate debtors to prioritize your invoice.

For example, a FMCG business in Makkah can offer a 2%–5% discount if the retailer settles the invoice within 10 days, encouraging faster cash recovery.

Unresolved disputes can delay an entire payment. Address any issues with products, services, or invoices immediately to remove barriers to payment and prevent the debt from escalating.

For instance, a construction materials business in Dammam can resolve invoice disputes by reviewing delivery records within 24 hours and issuing a corrected invoice the same day, helping contractors settle payments without delay.

Maintain a comprehensive, timestamped log of all calls, emails, negotiations, and agreements. It creates a clear, legally sound trail that is essential if disputes arise or legal action is required.

Is your Hejaz-based business struggling to track conversations, approvals, and invoice disputes across teams and locations?

Saudi-based firms have seen a 30% increase in productivity after using HAL Timesheets by giving managers real-time visibility into task completion, document tracking, and client communication logs.

Track team progress, enhance project profitability, and simplify client invoicing, all in one platform.

Also Read: Top Accounting Software for Small Businesses

If in-house efforts fail to yield results after 60-90 days, consider outsourcing the debt to a professional collection agency. These specialists have the expertise and resources to escalate the process while adhering to regulatory guidelines.

When all other options are exhausted, a formal legal notice or lawsuit may be necessary. This step can be costly and time-consuming, so ensure you have all documentation in order to strengthen your case.

When SMEs apply these strategies with discipline, they don’t just recover old payments; they build habits that prevent future debt, stabilize liquidity, and preserve relationships with high-value clients.

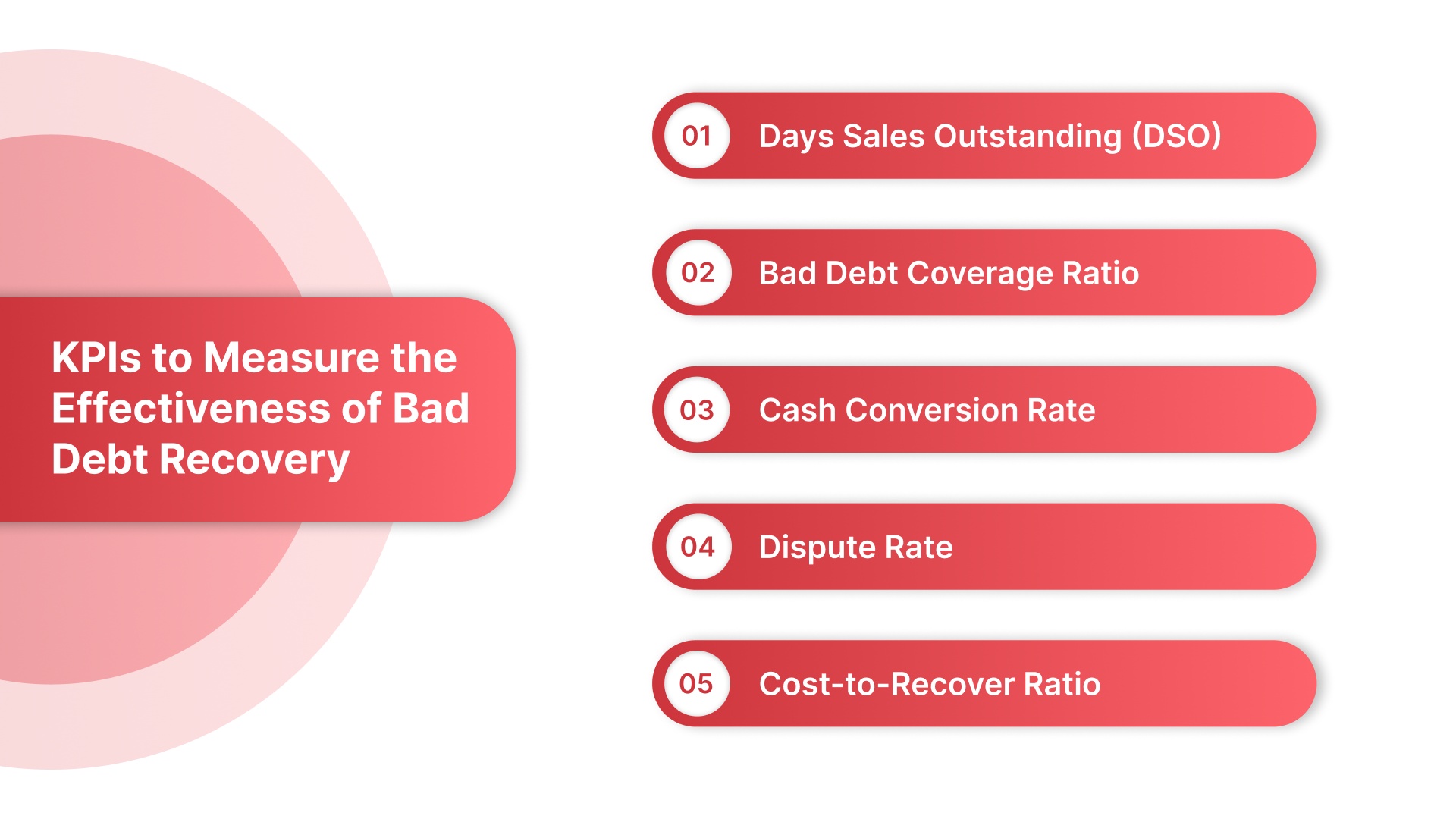

Yet, there are KPIs you should track to know whether your efforts are actually working.

Recovering bad debt is not just about collecting overdue payments; it is about measuring whether your recovery efforts actually strengthen cash flow and reduce financial risk.

SMEs in Saudi Arabia, especially those operating with tight credit cycles, need clear visibility into performance to improve decision-making.

Below are a few essential KPIs that help assess how efficiently your business is converting overdue receivables into cash and how well you’re preventing future write-offs.

Recommended Reading: How to Calculate Breakeven Point: A Simple Guide

Tracking these KPIs ensures you are not simply collecting debt, but doing it in a way that improves margins, strengthens cash flow, and reduces risk.

However, SMEs might still face challenges when trying to improve these numbers, because metrics only matter if you can realistically move them.

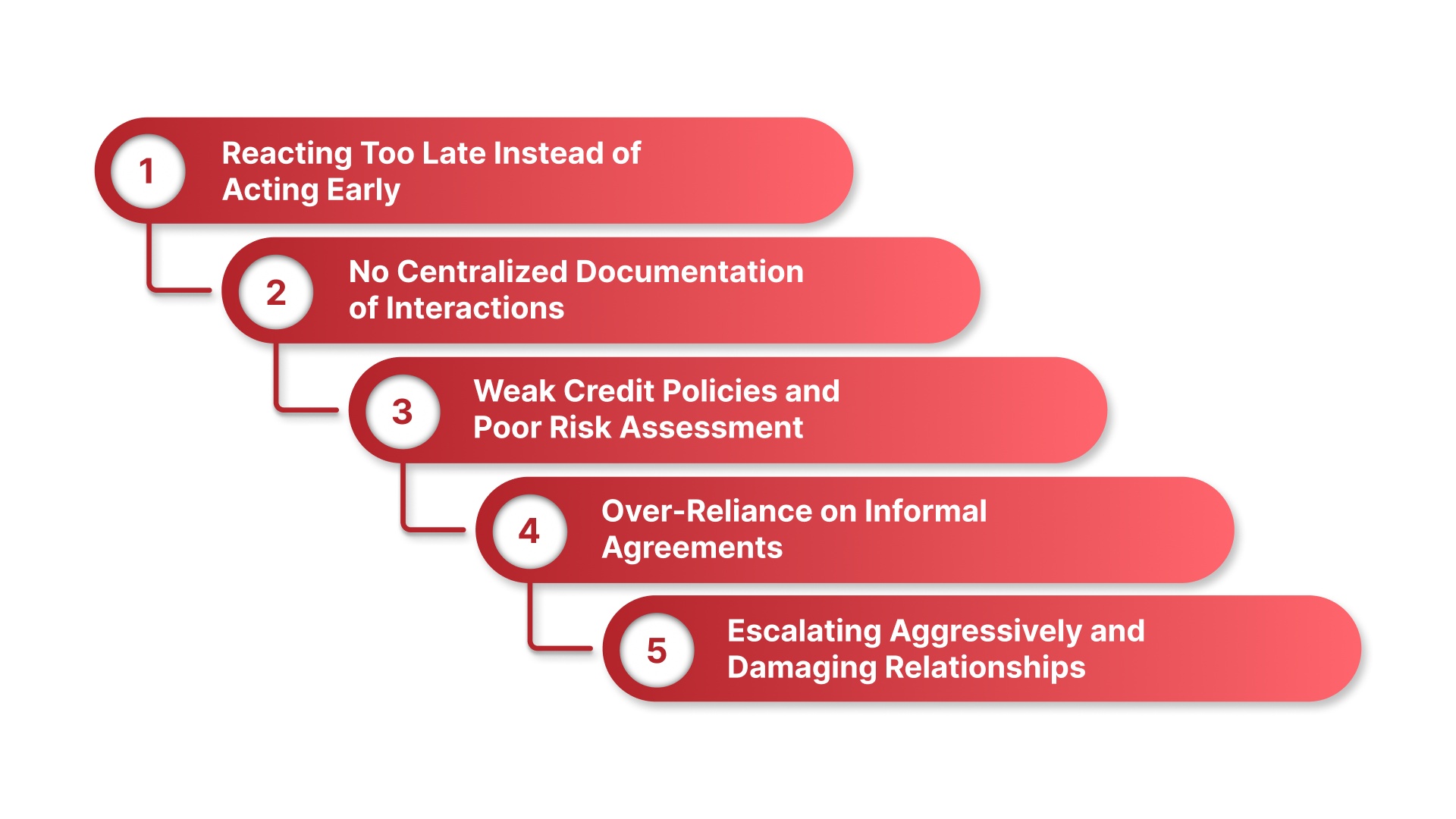

Many SMEs don’t fail because customers refuse to pay; they struggle because internal processes, follow-ups, and risk controls are inconsistent or reactive. In sectors with tight competition and thin margins, these gaps can turn manageable delays into severe financial stress.

A 2023 report by Monsha’at shows that late payments are the single biggest cause of cash flow disruption for SMEs in Saudi Arabia. This is especially true in construction, wholesale, and facility management, where payment terms often stretch beyond 90–120 days.

Below are a few common mistakes SMEs make when recovering bad debt and ways to avoid them before they turn into long-term losses:

Implement faster triggers, start reminders before due dates, not after. Use structured timelines: friendly reminders at 7, 15, and 30 days, followed by escalation. Early engagement increases recovery probability while relationships are still healthy.

Maintain detailed logs with timestamps: calls, emails, promises, disputes, and settlements. Documentation helps maintain accountability and supports legal recovery if needed.

Run credit checks, request guarantees, and establish clear approval thresholds. Tie credit limits to data average invoice size, historical payment time, and sector risk levels.

Formalize agreements: payment deadlines, late fees, dispute procedures, and communication channels. Clear terms reduce opacity and build professional expectations from day one.

Use a tiered approach: empathy with firmness. Focus on solutions first: payment plans, settlement discounts, or phased repayment. Keep legal escalation as a last resort.

Further Insight: 6 Successful Project Estimation Techniques

Bad debt recovery is rarely lost because debtors vanish; it’s lost because businesses lack consistent processes, documentation, and negotiation systems.

As companies mature, they inevitably ask: “How do we put all of this into a scalable system so we don’t repeat the same mistakes?”

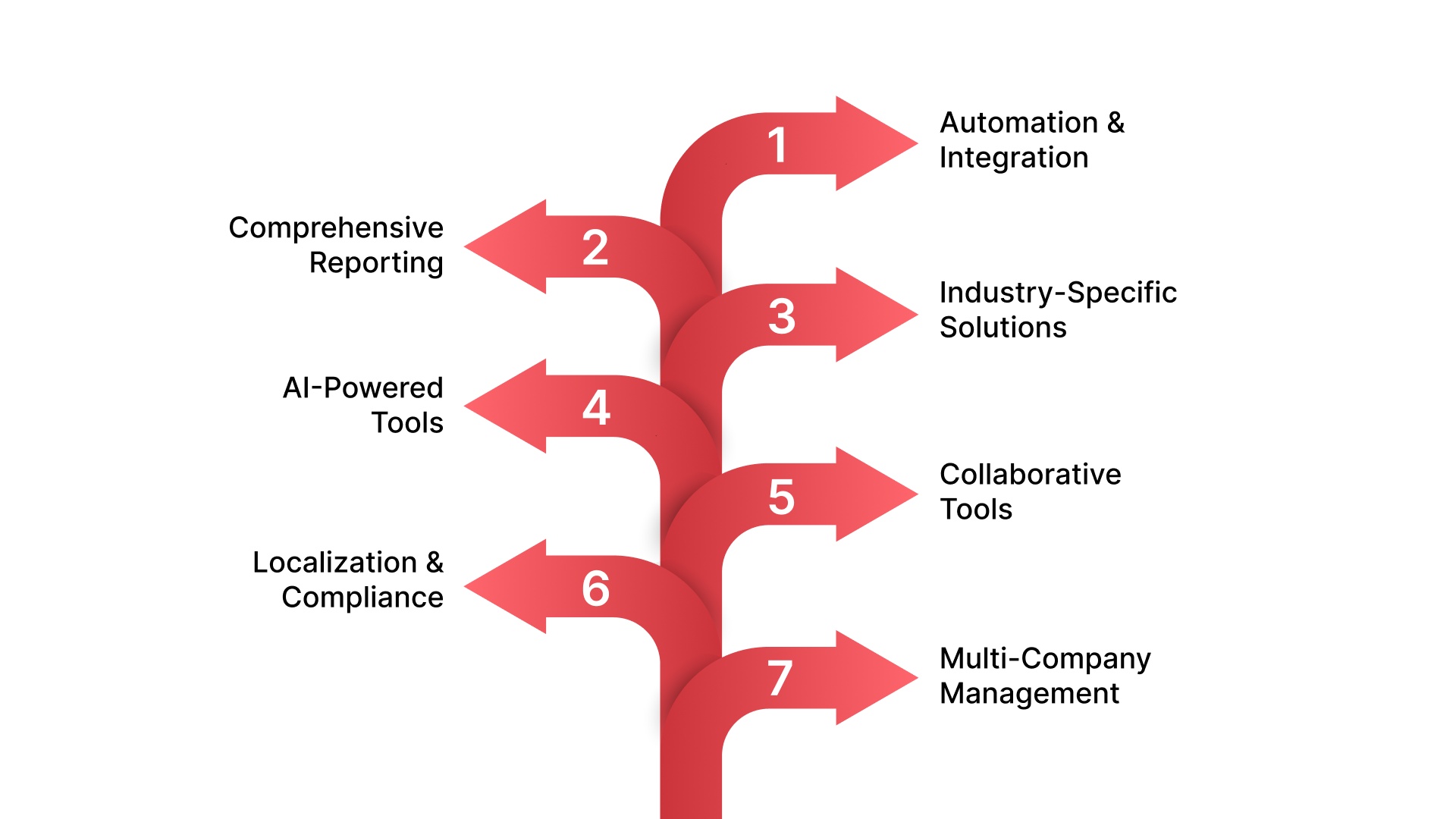

That’s why modern Saudi businesses are looking forward to modern ERP tools, helping teams automate, monitor, and simplify recovery without burning time or relationships.

HAL ERP is an advanced enterprise software designed to automate and unify operations across finance, sales, procurement, production, and service. It serves growing businesses and decision-makers: CEOs, CFOs, and operations teams in sectors like manufacturing, contracting, trade, and education.

With a customer-centric approach and fast implementation of 8–12 weeks, HAL helps organizations scale with confidence.

Below are key features that help SMEs prevent cash flow disruptions and reduce bad debt risk in real time:

HAL ERP’s key advantage isn’t just technology; it’s clarity. When Saudi SMEs can see their financial reality in real time, enforce policies automatically, and cut operational delays, cash flow improves naturally, and bad debt becomes a calculated exception, not a recurring crisis.

Jash Holding Company, a large multi-subsidiary organization, struggled with scattered project data, manual payroll for over 4,000 employees, and inefficient control of 12,000+ assets. Financial consolidation was slow, and the lack of bilingual system support created communication barriers.

After adopting HAL ERP, the company achieved over 60% gains in operational efficiency, reduced manual data entry, improved project cost visibility, and introduced faster, data-driven decision-making across subsidiaries.

Are you tired of juggling disconnected systems that slow down decisions, create errors, and drain productivity every single month?

%20(3).png)

Bad debt remains one of the most persistent threats to SME survival, especially in markets like Saudi Arabia, where long payment cycles and rising operational costs strain liquidity. SMEs struggle with recovery because of inflation, weak credit controls, delayed invoicing, and the pressure to extend terms to stay competitive, often at the cost of predictable cash flow.

To overcome these challenges, SMEs must adopt structured recovery strategies such as prompt invoicing, personalized communication, flexible repayment plans, payment incentives, and credit checks. When applied consistently, these strategies reduce overdue receivables, protect working capital, and improve long-term financial stability.

Monitoring key KPIs, like DSO, cash conversion cycle, dispute rate, coverage ratio, and cost-to-recover, helps assess progress, while avoiding common mistakes such as poor documentation, reactive collection, and weak credit policies, which prevent recurring losses. Becoming data-driven, proactive, and disciplined is essential for bad debt recovery.

Before closing, ask yourself: Are overdue invoices quietly corrupting your margins, delaying growth, and creating avoidable stress? Book a free demo with HAL and see how you can build financial discipline, strengthen cash flow, and take control of your operations today.

1. What are the common causes of bad debt in SMEs?

Bad debt often occurs when businesses extend credit without proper evaluation, rely on long payment terms, or fail to follow up promptly. SMEs also face bad debt due to disputed invoices, weak documentation, and customer cash flow issues. Strong policies can significantly reduce the risk of bad debt accumulation.

2. How can SMEs reduce bad debt without damaging customer relationships?

SMEs can reduce bad debt by setting clear payment terms, offering flexible plans, and communicating professionally. Early reminders, transparency, and dispute resolution help maintain trust. A customer-centric approach increases cooperation while keeping bad debt under control, especially in long-term business relationships.

3. How does ERP help SMEs improve financial control and prevent bad debt?

An ERP system centralizes invoicing, credit control, reporting, and follow-ups, making financial management proactive. Automated workflows, real-time dashboards, and alerts help reduce overdue accounts, prevent errors, and improve cash flow visibility. It reduces the likelihood of unpaid invoices turning into bad debt due to oversight.

4. Does Saudi ZATCA compliance help reduce bad debt for SMEs?

ZATCA-compliant e-invoicing improves financial transparency, speeds up verification, and minimizes disputes, which indirectly reduces bad debt risk. Standardized invoice data, automated validation, and audit trails make payments traceable. While ZATCA doesn’t eliminate bad debt, it promotes disciplined financial processes.

5. What KPIs should SMEs track to monitor bad debt performance?

Important KPIs include Days Sales Outstanding (DSO), dispute rates, aging buckets, recovery cost, and write-off ratios. These indicators help SMEs identify rising bad debt, understand cash flow risk, and evaluate collection performance. Regular tracking enables corrective action before bad debt becomes unmanageable.