Struggling to assess your company's financial health? Revenue, often referred to as the top line on the income statement, is your first step toward understanding your business's profitability and growth potential.

Official statistics revealed that the operating revenues of the business sector in Saudi Arabia in the previous years exceeded 4 trillion riyals ($1 trillion). This demonstrates the significant role that revenue plays in driving the country's economic growth.

In this guide, we'll break down the definition of revenue, its importance, how to calculate it, and how understanding revenue can help optimize your strategies.

At its core, revenue is the total income your company generates from selling goods and services before deducting any expenses. It's often referred to as the "top line" on your income statement, and it's the starting point for measuring a company's financial performance.

Key Points About Revenue:

For Saudi businesses, especially those operating in the manufacturing or retail sectors, revenue plays a pivotal role in assessing the potential for scaling operations and achieving profitability.

Revenue is more than just a figure; it's a crucial indicator of your business's growth potential, financial health, and profitability. Here's why tracking revenue is vital for any business:

Understanding how to calculate revenue is crucial for businesses in Saudi Arabia. Here are the basic formulas based on whether you sell products or services:

Example: If a retail business in Riyadh sells 2,000 units at an average price of SAR 50, their total revenue would be: 2,000 × 50 = 100,000 SAR (Revenue)

Plus 15% VAT = 115,000

Example: A law firm offering legal services to 300 clients at SAR 500 each would have a revenue of: 300 × 500 = 150,000 SAR (Revenue)

This simple yet effective revenue formula helps you assess how well your business is performing, which is essential for making future decisions.

Understanding when to record revenue is just as important as knowing how much revenue to report. The Revenue Recognition Principle under Generally Accepted Accounting Principles (GAAP) specifies when revenue should be recognized, ensuring that financial statements reflect the actual economic activity of a business.

Here are the key situations when revenue is recognized:

Revenue is recognized when the ownership of goods or services is transferred to the buyer, signifying the point at which the risks and rewards of ownership pass to the customer. This transfer doesn't always depend on the physical delivery of goods but rather on when the buyer gains control over the asset.

Example: A real estate developer in Saudi Arabia, such as Dar Al Arkan, sells residential units under contract. Revenue is recognized once the buyer gains control of the property through contract transfer, even if the handover or final payment occurs later, because the ownership risks and benefits have already shifted to the customer.

For service-based businesses, revenue is recognized when the service is fully delivered. This differs from the sale of goods, where the transaction is considered complete when the product changes hands. With services, the recognition happens as the service is provided over time, typically aligning with performance milestones or specific deliverables.

Example: A Riyadh-based consultancy firm, such as KPMG Saudi Arabia, is contracted to provide advisory services for a Vision 2030 infrastructure project over 12 months. The firm recognizes revenue monthly as each phase of the advisory work is completed, even though the client may have paid the full contract value upfront.

Revenue recognition occurs even when payment is not received upfront. When a sale is made on credit, the business recognizes the revenue at the point of purchase, not when the customer pays. This transaction is recorded as accounts receivable, indicating that the company has a legal right to receive payment for the goods or services provided.

Example: A Saudi software provider, such as Solutions by STC, signs a multi-year licensing agreement with a government agency for its enterprise software. The revenue is recognized at the start of the contract, even though the agency will pay in installments over the contract term, once the license is granted. The unpaid balance is recorded as accounts receivable.

Also Read: Financial Statements: The Cornerstone of Effective Business Management

In Saudi Arabia, understanding and calculating revenue is not only crucial for financial reporting but also for ensuring compliance with local regulations such as ZATCA e-invoicing, Zakat, and IFRS 15. The local legal framework requires businesses to adhere to specific guidelines when recognizing and reporting revenue, which can impact a company’s tax obligations and overall financial health.

The Zakat, Tax, and Customs Authority (ZATCA) has implemented Phase 2 of its e-invoicing program, which took effect in December 2021. Under this phase, businesses are required to generate electronic invoices for all transactions, which must comply with Saudi VAT regulations. This has a direct impact on how revenue is reported and tracked.

Businesses must ensure that their revenue recognition processes are integrated with the e-invoicing system, as all invoices—whether for goods, services, or contracts—must be issued electronically, and VAT must be correctly calculated. This ensures real-time reporting and compliance with the Saudi VAT law.

Example: A company like Almarai, a leading dairy and food manufacturer, sells its products to retailers across Saudi Arabia. When a retailer purchases products, Almarai must generate an electronic invoice that accurately reflects the sale, including VAT charges. The company’s HAL ERP system automates this process, ensuring all invoices comply with ZATCA’s e-invoicing standards, enabling seamless VAT reporting.

Zakat is an essential aspect of Saudi Arabia’s tax system, and businesses must be aware of how it is calculated. While Zakat is generally based on a company's net income, the calculation base for Zakat is different from that of income tax in other countries.

The Zakat calculation typically considers a company's net assets, but the base for calculating it may differ depending on whether revenue or net income is used. For many companies in Saudi Arabia, Zakat is calculated on gross revenue, and businesses must adjust their revenue reporting to reflect the impact of Zakat.

Example: A construction company like Saudi Binladin Group must calculate Zakat based on its revenue from projects, even though the company's net income might be lower due to high operating costs and expenses. Zakat is paid on the gross revenue from these projects, ensuring compliance with the Kingdom's tax framework.

The Saudi Organization for Certified Public Accountants (SOCPA) has adopted IFRS 15—the international accounting standard for revenue recognition. This standard governs when and how revenue should be recognized, focusing on the transfer of control of goods or services to the customer.

For Saudi businesses, this means that revenue must be recognized based on performance obligations in contracts, which can impact the timing and amount of revenue reported, especially in industries with long-term contracts. The IFRS 15 standard has implications for construction, real estate, and service-based industries in Saudi Arabia, where contracts span several months or years.

Example (Saudi context): A Saudi real estate developer, such as Red Sea Global, signs long-term contracts for the development of luxury resorts. According to IFRS 15, revenue from the sale of real estate properties is recognized progressively over the course of the development, in line with performance milestones. This ensures that revenue recognition aligns with the actual delivery of services and construction stages, ensuring transparent financial reporting.

Let's look at some practical examples of revenue in different sectors:

In Saudi Arabia's contracting industry, businesses like Coastline LLC leverage HAL ERP to automate invoicing and track revenue in real-time, ensuring quick invoicing and on-time payments for services provided.

The accrual basis of accounting is a method that ensures revenue is recognized when earned, not when cash is received. This approach is essential for businesses that need a more accurate representation of their financial health. Under this method, transactions are recorded as soon as they occur, whether or not cash has been exchanged.

When calculating revenue, the accrual basis of accounting ensures you account for earned revenue, not just cash received. This means that revenue is recognized as soon as a service is performed or a product is delivered, even if the customer hasn't paid yet. Similarly, expenses are recorded when they are incurred, not when they are paid.

By aligning revenue and expenses to the period they occur, the accrual method gives a more realistic picture of a business's financial performance.

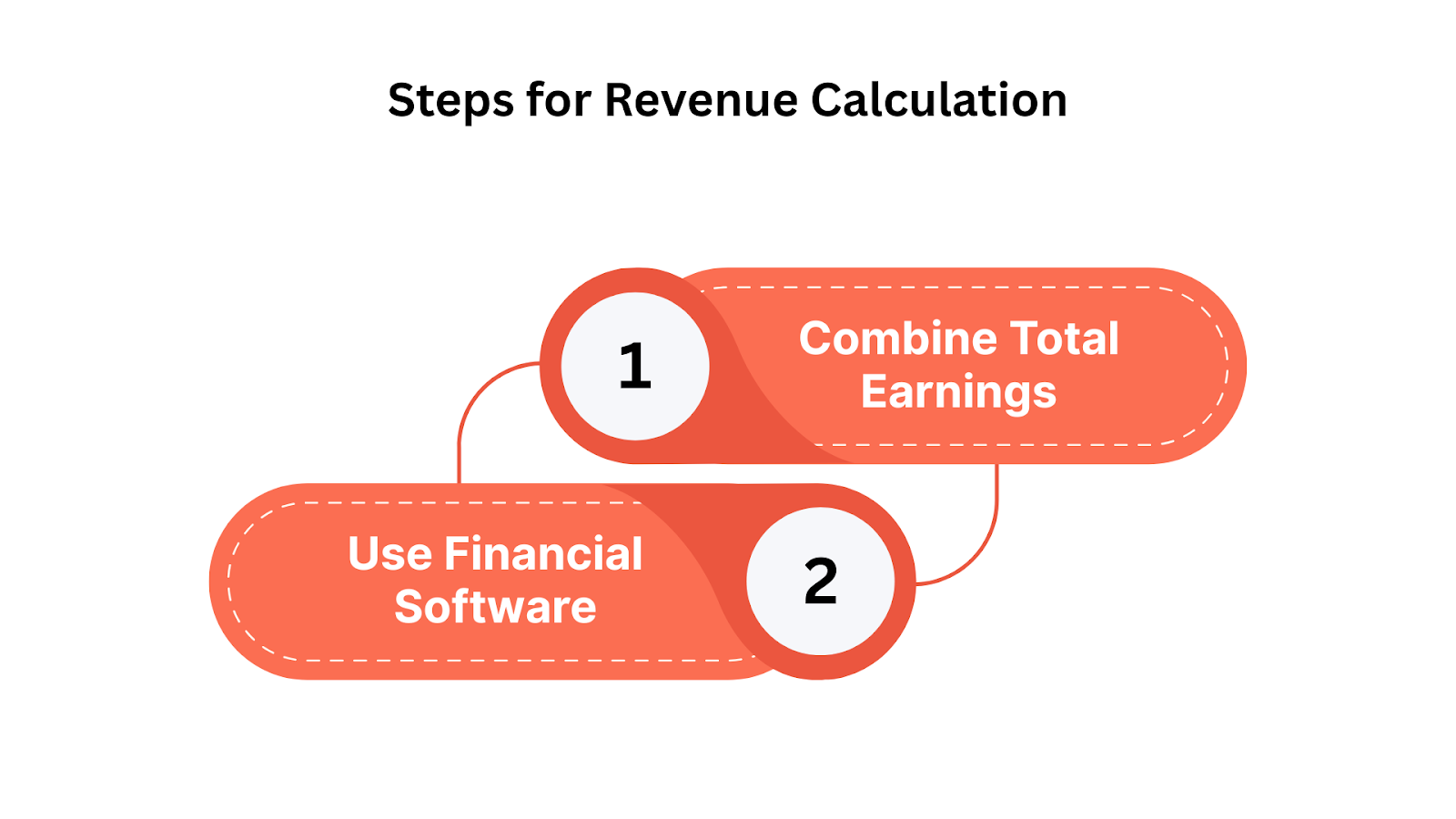

Steps for Revenue Calculation:

This step involves adding up all the amounts earned from sales, whether the payment has been received or not. This includes both cash transactions and sales on credit.

Example:

Imagine a retail store makes three sales:

The total earnings in this case would be SAR 2,000 + SAR 3,000 + SAR 1,500 = SAR 6,500, even though some payments are yet to be received.

Many businesses use financial software to automate revenue calculations, track payments, and ensure compliance with local regulations, especially in regions like Saudi Arabia, where regulatory requirements like ZATCA E-invoicing apply. Tools like HAL ERP help businesses streamline the process, ensuring accurate revenue reporting and regulatory compliance.

Example: Consider Al Haram Retail Chain, a large retail company in Saudi Arabia. Al Haram implemented HAL ERP to automate its revenue calculations and streamline operations. The software allowed the company to track revenue across multiple locations, including sales on credit. For instance, when a customer at one of the retail outlets made a purchase worth SAR 5,000 on credit, HAL ERP automatically recorded the transaction, updated accounts receivable, and calculated the VAT according to Saudi regulations.

The accrual method also helps businesses avoid errors that can arise from delayed payments or missed invoices, ultimately reducing financial risk.

Understanding and analyzing revenue is critical for making informed business decisions. By examining revenue data, businesses can:

Also Read: Understanding Profit and Loss Statement Basics and Examples

HAL ERP offers a comprehensive solution to streamline revenue calculation, making it easier for businesses in Saudi Arabia and beyond to stay compliant with local regulations and ensure financial accuracy. With its advanced automation features, HAL ERP helps businesses efficiently track revenue, manage credit sales, and automate reporting for better financial management.

Key Features of HAL ERP for Revenue Calculation:

Want to see how HAL ERP optimizes revenue tracking in real-time? Explore the success stories from businesses that have transformed their financial processes using HAL ERP.

Understanding revenue is vital for any business seeking to thrive in today's competitive landscape. Whether you're a retailer, a service provider, or a manufacturer, tracking and analyzing revenue accurately will provide you with invaluable insights into your company's financial performance. HAL ERP offers seamless solutions for managing revenue, automating processes, and staying compliant with local regulations, helping your business grow.

Contact us today to schedule a free, tailored demo and discover how HAL ERP. can help you simplify operations, improve efficiency, and boost your bottom line.

Q. What does revenue mean?

A. Revenue refers to the total income generated by a business from its normal business activities, such as sales of goods or services. It represents the top line or gross income, before expenses, taxes, or other deductions are applied.

Q. What is revenue or profit?

A. Revenue is the total amount a company earns through sales of goods or services. Profit, on the other hand, is the amount left after all expenses (cost of goods sold, taxes, etc.) are deducted from revenue, representing the company's actual earnings.

Q. What is the difference between revenue and turnover?

A. Revenue and turnover are often used interchangeably. Still, turnover typically refers to the total sales a company generates in a specific period. In contrast, revenue can include other sources like interest and royalties, making turnover more focused on sales volume.

Q. What is a formula for revenue?

A. The formula for revenue is:

Revenue = Price per Unit × Quantity Sold

This formula calculates the total income by multiplying the selling price of a product by the number of units sold during a given period.