Have you ever wondered how businesses track their financial health or how decisions are made based on numbers?

Accounting is the backbone of every successful business, offering a clear picture of where money is coming from and where it's going.

Understanding accounting basics can unlock the door to financial insight, whether you're a budding entrepreneur, a student, or simply someone looking to understand how finances work.

From balancing budgets to managing expenses, accounting is more than just numbers on a page; it's the language of business.

In this article, you will learn about the basics of accounting, key financial statements, and fundamentals to help you grasp the essentials. Let’s uncover it!

Accounting is the process of recording, analyzing, and interpreting financial transactions for a business. The basics of accounting encompass understanding key concepts, including revenue, expenses, assets, liabilities, and equity.

Business accounting involves the continuous tracking, analysis, and understanding of a company's financial activities. Entrepreneurs use accounting data to monitor financial obligations and make informed decisions that lead to stronger, more sustainable business operations.

While knowing the basics of accounting is crucial, it’s essential to seek professional advice from an accountant or bookkeeper and consult a tax practitioner when dealing with tax-related matters.

Accounting is essential not only for budgeting but also for building trust with stakeholders. Investors rely on financial reports to assess the health and potential of a business, while creditors use the data to evaluate a company’s ability to repay loans.

Accurate and regular reporting also ensures compliance with tax regulations, helping businesses avoid legal issues.

Understanding accounting fundamentals involves key terms that describe essential concepts in business finances:

To keep finances organized, businesses use a chart of accounts to categorize financial data under key accounts. These accounts include:

Also Read: Financial Accounting Made Simple: Principles, Types, and Key Functions

Below, you will explore some of the key aspects of accounting basics that you must understand to grasp the concept better.

Financial statements are essential tools for assessing a company's financial health. They provide insights into the company's performance, position, and cash flow. Below are the key types of financial statements that businesses in Saudi Arabia commonly use, along with examples to illustrate how each is prepared:

The income statement summarizes a company’s revenues and expenses over a specific period, calculating the net profit or loss for that time.

Key Features:

Example: For a company with SAR 1,875,000 in sales and SAR 1,125,000 in expenses for a quarter, the income statement would show a net profit of SAR 750,000.

Account Types:

The balance sheet provides a snapshot of a company’s financial position at a specific point in time, listing its assets, liabilities, and shareholders’ equity.

Key Features:

Example: If a company has SAR 4,000,000 in assets, SAR 2,400,000 in liabilities, and SAR 1,600,000 in equity, the balance sheet would show these figures as equal, maintaining the fundamental accounting equation.

Account Types:

The cash flow statement tracks the movement of cash into and out of the business, adjusting for non-cash expenses and changes in working capital.

Key Features:

Example: If a company had SAR 1,125,000 in operating cash inflows, SAR 375,000 in investing cash outflows, and SAR 187,500 in financing cash inflows, the cash flow statement would reflect these movements, helping assess liquidity.

Account Types:

The P&L statement summarizes the business’s income and expenses over a specific time frame to assess profitability.

Key Features:

Example: A company generates SAR 2,250,000 in income, has a cost of goods sold (COGS) of SAR 937,500, and incurs operational expenses of SAR 375,000. The P&L statement would show a net profit of SAR 937,500.

Account Types:

The trial balance is a preliminary financial report that lists all ledger accounts and their balances at a specific point in time. It is used to confirm that total debits equal total credits, ensuring accuracy in bookkeeping before preparing the financial statements.

Key Features:

Example: A construction supply store in Riyadh prepares its monthly trial balance showing debits: cash (SAR 200,000), accounts receivable (SAR 125,000), and inventory (SAR 175,000), totaling SAR 500,000. The credits include accounts payable (SAR 100,000), a bank loan (SAR 150,000), and owner’s equity (SAR 250,000), also totaling SAR 500,000. Since debits equal credits, the trial balance is accurate and ready for financial statement preparation.

Account Types:

Each of these financial statements provides valuable insights into a company’s financial health. They help businesses like yours in Saudi Arabia assess performance, understand assets and liabilities, and monitor cash flow.

Also Read: Understanding the Importance and Types of Accounting Standards

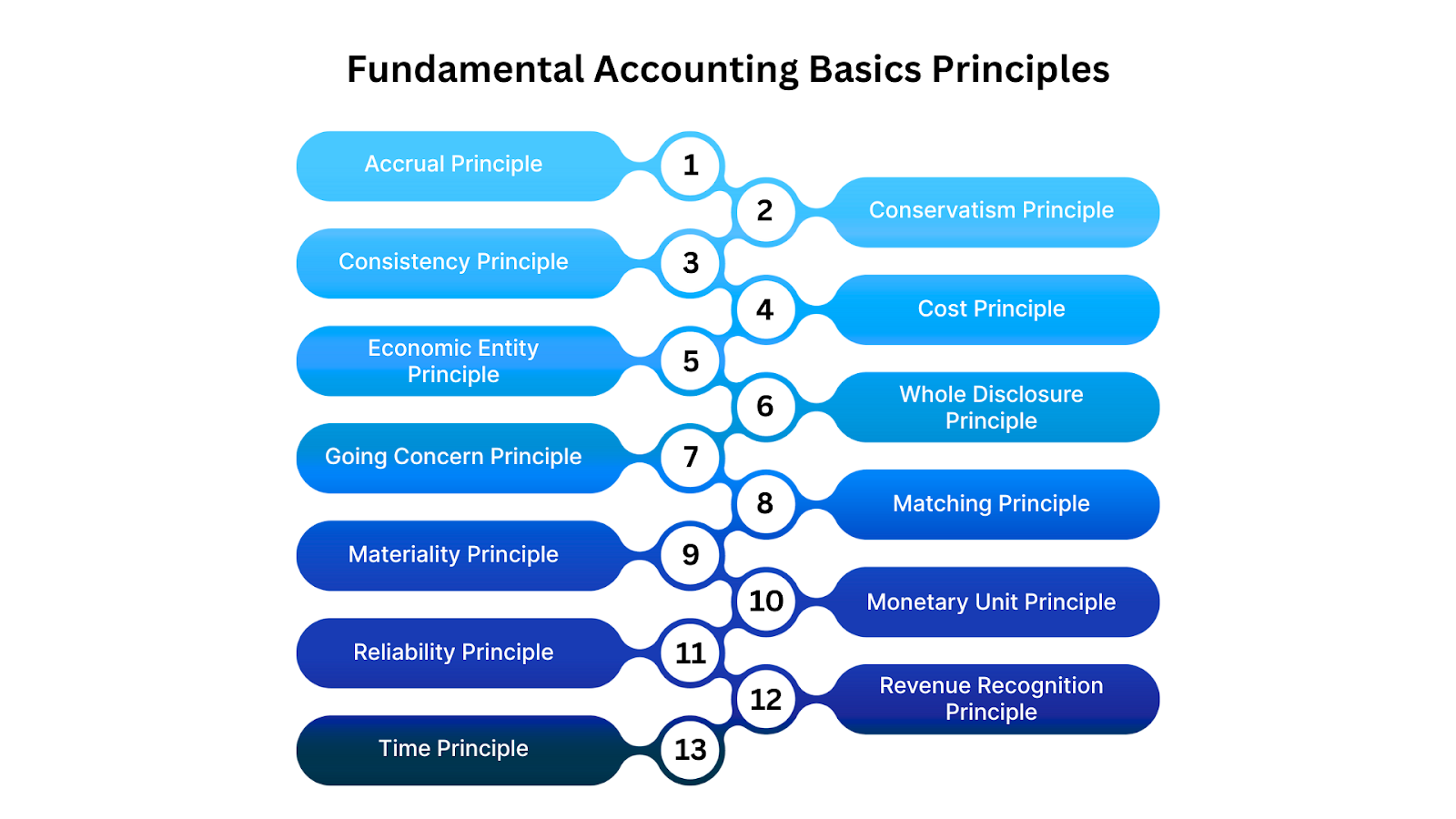

Now, below you will uncover fundamental accounting basics principles

Accounting principles are fundamental rules that guide businesses in reporting their financial information. Below are some core principles that provide structure to accounting practices:

These principles help standardize financial reporting, ensuring that businesses produce reliable, comparable, and accurate financial statements. Below are the basic accounting terms.

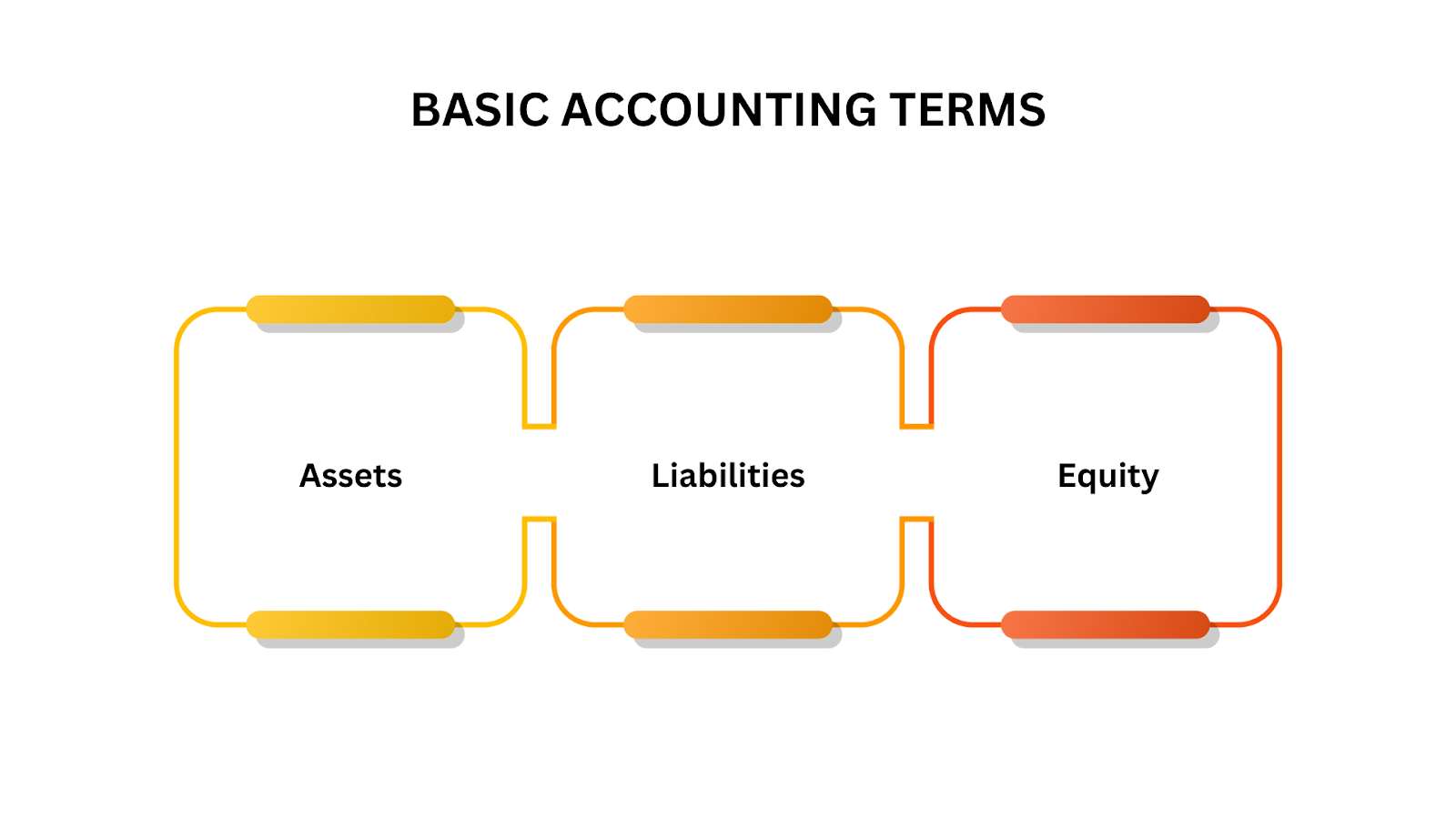

Grasping basic accounting terms, such as assets, Liabilities, and Equity, is crucial for understanding how businesses manage and assess their financial health. Below is an in-depth explanation of these terms, including how they are calculated:

Assets are economic resources owned by a business that are expected to provide future financial benefits. These can include both tangible items, such as cash, inventory, buildings, and equipment, and intangible assets, such as patents and trademarks.

Example:

How it’s Calculated:

Assets can be calculated using the formula:

Liabilities are debts or obligations that a business owes to outside parties. These include loans, accounts payable, mortgages, and other financial obligations.

Example:

How it’s Calculated:

Liabilities can be calculated by summing both current and non-current obligations:

Equity represents the owner’s residual interest in the business's assets after deducting its liabilities. It is often referred to as the company's net worth. Equity is crucial for assessing the financial stability and value of a business's ownership.

Example:

How it’s Calculated:

Equity is calculated using the fundamental accounting equation:

For instance, if a business has SAR 500,000 in assets and SAR 300,000 in liabilities, the equity would be:

This means the company’s owners have SAR 200,000 in residual value after settling all liabilities.

By understanding these basic accounting terms and how to calculate them, you can better interpret a company’s financial position and make informed decisions based on its financial health.

Also Read: Financial Statements: The Cornerstone of Effective Business Management

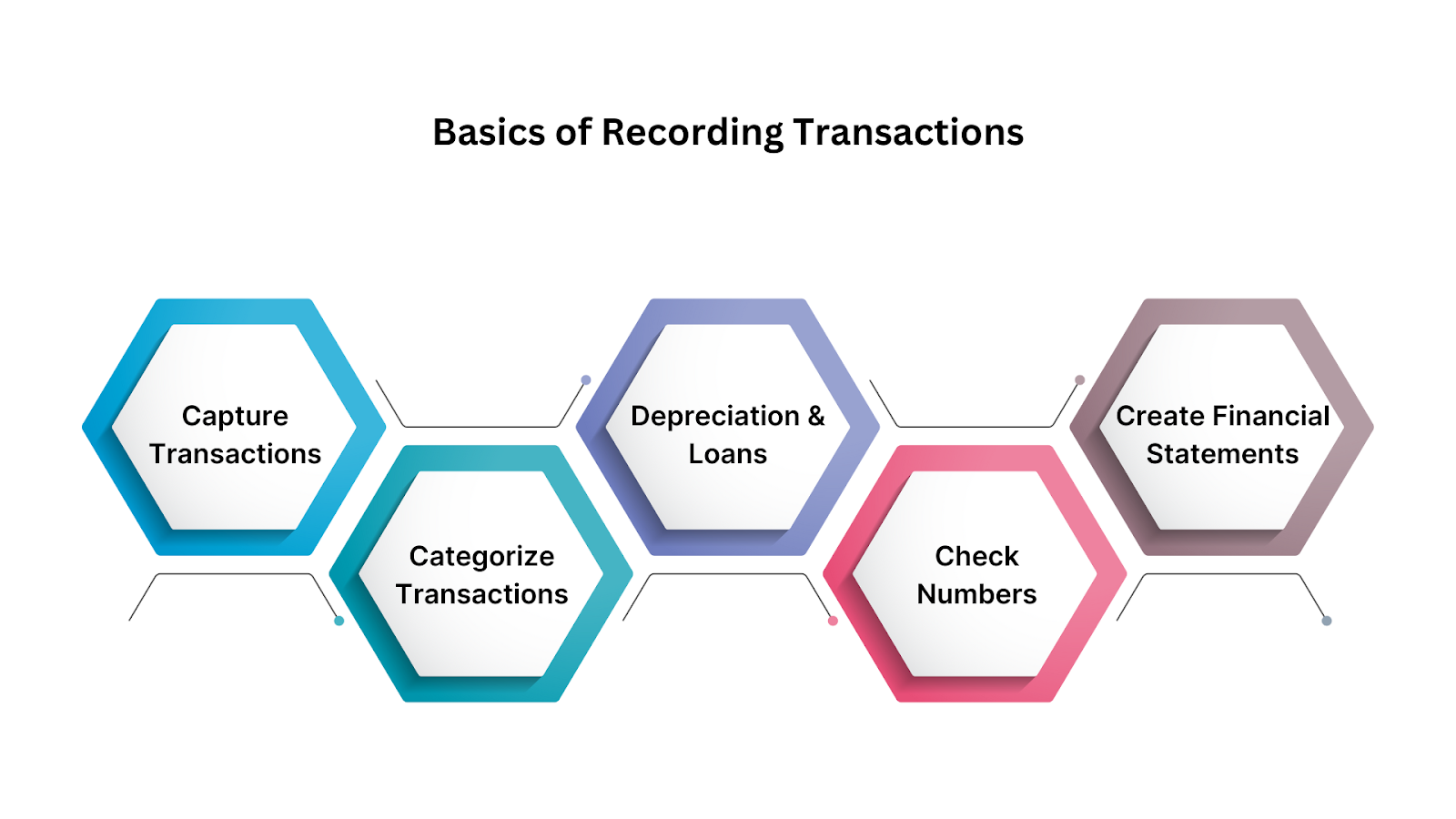

Once you have a grasp of these key terms, it's essential to understand the Basics of Recording Transactions that you will explore below.

Recording transactions is a fundamental process for tracking all financial activities in your business, such as sales, expenses, loans, and investments. This practice is essential for understanding your business’s financial position, allowing you to determine whether you’re making a profit, who owes you money, and if you’re able to meet your financial obligations. Proper transaction recording also supports informed decision-making and helps maintain compliance with tax regulations.

Here’s a more detailed breakdown of how to effectively record transactions:

The first step is ensuring that all financial transactions are recorded accurately. This includes sales, expenses, receipts, bank deposits, and any other monetary movements. To streamline this process, use business-specific bank accounts and accounting software, which can automatically import and categorize transactions. This reduces human error and ensures no transaction is missed.

Example: If you sell a product worth SAR 500, ensure the sale is recorded in your accounting software and backed up by the invoice or receipt.

Once transactions are captured, they must be classified into appropriate categories for easier financial analysis and reporting. Key categories include:

By assigning each transaction to the right category, you ensure your financial statements reflect an accurate picture of your business’s financial performance.

Example: A SAR 10,000 utility bill would be categorized under "Utilities" as part of operating expenses.

For long-term assets, such as machinery, vehicles, or office equipment, you need to record depreciation to reflect the asset’s reduction in value over time. Additionally, loans should be carefully tracked by separating principal repayments from interest payments. Depreciation and loan handling ensure that your balance sheet accurately reflects the value of assets and liabilities.

Example: If you purchase machinery for SAR 50,000, you’ll need to depreciate its value over several years, which will impact your financial reports. Similarly, if you repay a SAR 5,000 loan, part of the payment will be applied towards the principal, and the rest will be applied towards the interest.

Regular reconciliation of your accounting records with your bank statements is vital to ensure the accuracy of your records. This step helps identify discrepancies, such as missing transactions or data entry errors. Timely reconciliations also provide an up-to-date view of your business's cash flow and financial position.

Example: You may find that your records show SAR 5,000 in bank deposits, but your bank statement shows SAR 4,800. This discrepancy should be investigated to ensure the numbers match.

Once transactions are recorded and categorized, you can generate financial statements, which give a comprehensive view of your business's financial health. Key statements include:

By creating these financial statements, you’ll gain valuable insights into your business’s performance, helping you make informed decisions and maintain financial stability.

Also Read: Saudi Businesses Rejoice! HAL Accounting Software Is Here To Revolutionize Your Finances

Below, you will explore the role of accounting software and why they are important.

Accounting software is no longer a luxury; it’s become a core part of how businesses manage their finances today. Whether you're running a Shopify store, selling on Amazon, or managing multiple income streams, the right tools can significantly reduce the manual work on your plate.

Here’s a closer look at what accounting software does, why it matters, and how it fits into modern business operations in the UK.

The real value of accounting software is in the time, energy, and errors it saves. Traditional accounting methods involved extensive manual data entry, cross-checking, and repetitive tasks. Now, much of that can be done with just a few clicks.

It handles everything from:

This gives accountants and business owners more time to focus on the bigger picture, like analyzing trends, planning for growth, and offering sound financial advice.

Also Read: How to Calculate Marginal Cost: Formula and Examples

By implementing effective transaction recording and financial management practices, your business can ensure accurate and timely financial insights. This is where the right accounting software comes in.

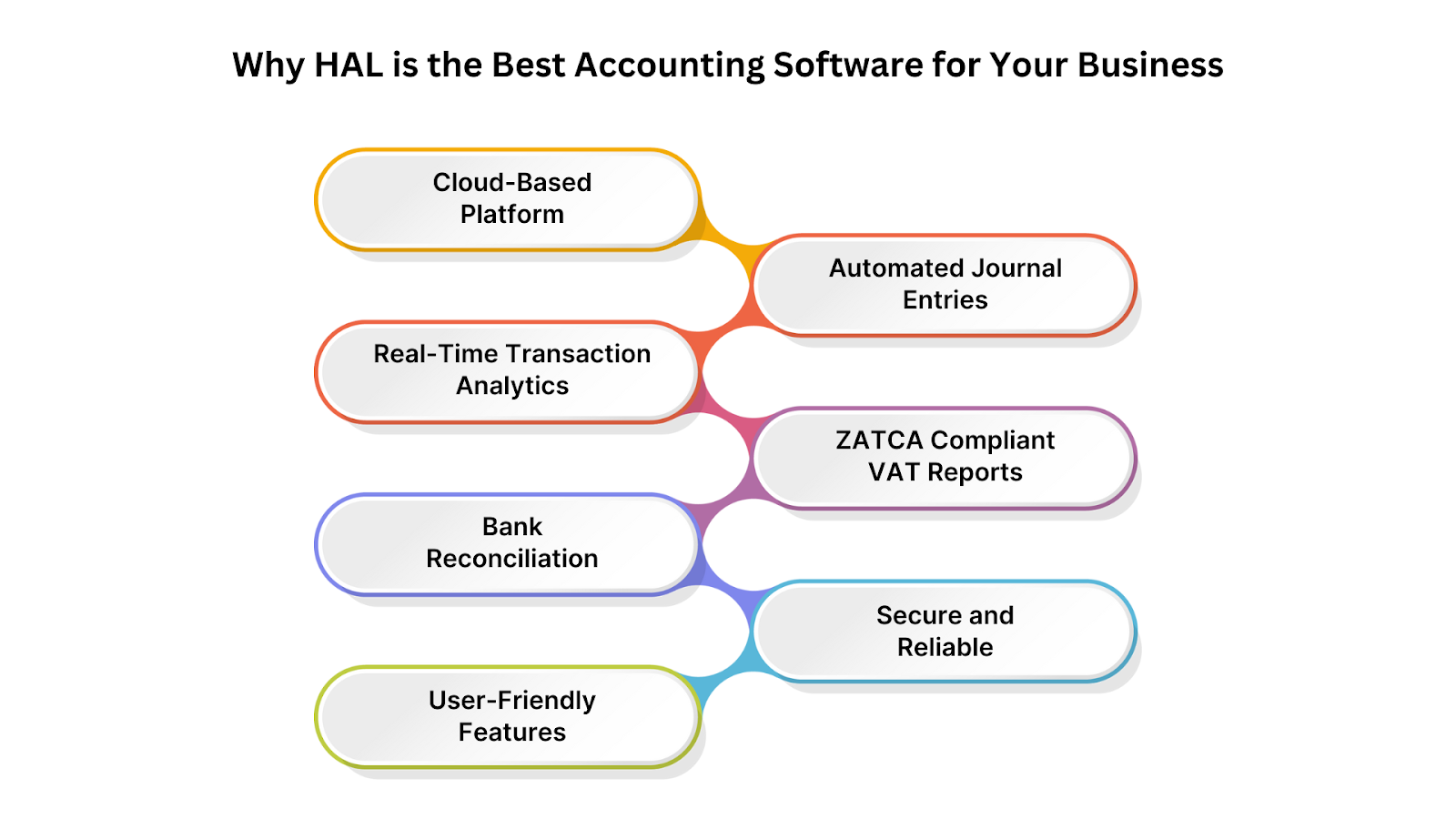

HAL is not just another accounting software; it’s a comprehensive, cloud-based solution designed to help businesses get more done in less time, with greater control and simplicity. Perfect for accountants who need robust features without the complexity, HAL provides everything from automated journal entries to real-time transaction analytics, all while ensuring ease of use.

Here’s why HAL stands out:

HAL is the ultimate solution for small and medium-sized businesses in Saudi Arabia, providing the tools you need to manage your finances efficiently and securely, without the hassle.

Also Read: Navigating the challenges of complying with ZATCA regulations

Now, you have landed on the last section of this article that will tell you the best practice to get started with accounting.

Starting is often the most challenging part, so here’s a simple checklist to get your accounting in order.

1. Set Up a Business Bank Account: Even if it’s not mandatory, opening a separate account for your business makes bookkeeping easier and helps avoid mixing personal and business transactions, especially when working with an accountant or bookkeeper.

2. Build a Chart of Accounts: This is the backbone of your financial records. It organizes your transactions into categories in your general ledger. Whether you're using spreadsheets or software, set this up early to stay organized.

3. Choose Your Accounting Method: When selecting an accounting method, you can choose between Cash Accounting and Accrual Accounting:

4. Record and Organize Transactions: Digital tools now make it easier to sort expenses without digging through piles of receipts. Still, keep all records, receipts, bills, invoices, and bank statements, especially those related to tax deductions.

5. Understand Your Tax Responsibilities: Familiarise yourself with the taxes applicable to your business and keep accurate records. Setting aside money in advance helps you avoid surprises during tax season.

6. Stay Compliant with Tax Laws: Effective daily bookkeeping ensures your business runs smoothly. Monitoring your income, expenses, and liabilities regularly helps spot issues early and ensures you're meeting tax requirements.

7. Set Up Invoicing and Payroll Early: Establishing these systems from the start saves time later. Tools like MYOB automate many of these tasks. Learn how to distinguish between employees and contractors to ensure legal compliance.

8. Reconcile Monthly: Review your bank accounts monthly to identify errors, fraud, or any unusual activity, especially if you manage multiple accounts.

9. Work with a Professional: When in doubt, talk to an expert. Whether it’s general advice, tax planning, or financial strategy, a professional can make a real difference.

To fully capitalize on your ERP and mold management strategy, you need an accounting system built for speed, compliance, and control.

After understanding accounting basics, the next step is choosing the right tool to manage them efficiently. That’s where HAL Simplify steps in your trusted partner for secure, compliant, and easy-to-use accounting in Saudi Arabia.

Built with ZATCA compliance and Saudi business workflows in mind, HAL gives you the tools to manage every part of your accounting from journal entries to VAT reports with speed, clarity, and control.

HAL makes accounting efficient, simple, and faster. With an Excel-like interface and bulk processing tools that save you time every day.

Why Saudi Businesses Prefer HAL:

Book a free demo with our subject matter expert in Saudi Arabia and see how HAL Simplify can streamline your workflows.

You have covered all the crucial aspects of accounting basics and have now reached the concluding section of this article, where you will receive a quick recap of what you explored.

Understanding accounting basics is essential for making informed financial decisions, whether you’re managing a small business or just starting. From grasping key principles and financial statements to using tools like HAL accounting software, you now have a clear path forward.

With the proper foundation, such as setting up a business bank account, selecting the correct method, and utilising reliable software, you’ll be in control from day one.

Stick to the basics, stay consistent, and don’t hesitate to seek expert help when needed. That’s how solid financial management begins.

Ready to simplify your accounting and take control of your finances? HAL makes it easy with automated entries, smart dashboards, and VAT-compliant reporting built in.

Whether you're just getting started or scaling quickly, HAL provides you with the tools to save time, reduce errors, and focus on what truly matters: growing your business. Book a free demo today and see how HAL can make your accounting smarter, faster, and stress-free.