Every business must keep financial records accurate and balanced to maintain trust and comply with regulatory requirements. Errors at this stage can delay reporting and create compliance risks that directly affect decision-making and audit outcomes.

In Saudi Arabia, maintaining accurate records carries additional weight due to SOCPA standards, ZATCA e-invoicing mandates, and VAT reporting obligations, which all require strict adherence. Vision 2030 also emphasises financial transparency and stronger governance, pushing companies to strengthen reporting practices across contracting, trading, and retail sectors.

In this blog, we will discuss the concept of a trial balance, its purpose, types, and the process of preparing it. We'll also examine its role in accounting, the differences between trial balances and balance sheets, and how businesses can benefit from efficient trial balance management.

A trial balance is a statement that lists all the accounts in the general ledger, along with their respective debit or credit balances. Its primary purpose is to check the arithmetical accuracy of the books by ensuring that the total of debit balances equals the total of credit balances. While the trial balance provides a snapshot of the financial standing, it’s important to note that a balanced trial balance doesn’t necessarily guarantee error-free financial statements. It simply confirms that the fundamental accounting equation (debits = credits) has been followed.

Also Read: Financial Statements: The Cornerstone of Effective Business Management

The preparation of a trial balance serves multiple important purposes in accounting:

Also Read: Top Accounting Software for Small Businesses in 2025

Now that we understand why a trial balance is beneficial, let's examine what distinguishes it from a balance sheet.

While both the trial balance and balance sheet are important financial documents, they serve different purposes. The trial balance is an internal tool used to verify that the debits and credits in the accounting system are balanced, while the balance sheet is an external document that provides a snapshot of a business’s financial position. Here’s how the two differ:

Now that we've explored the role of a trial balance and how it differs from the balance sheet, let’s dive into the types of trial balances used in accounting.

Trial balances can be classified into three main types, depending on the stage of the accounting process. Each type serves a unique purpose and is used at different stages of financial reporting.

The unadjusted trial balance is the first trial balance prepared during the accounting cycle. It includes all the ledger balances before any adjustments are made for accruals, depreciation, or other adjustments. This trial balance provides an initial check to see if debits and credits are in balance, but it is not the final version used for financial reporting.

Once adjustments have been made for accrued expenses, revenues, or other items, the adjusted trial balance is prepared. This version reflects the updated balances after adjustments, providing the final list of accounts that will be used to prepare the income statement and balance sheet.

The post-closing trial balance is prepared after all closing entries have been made. This type of trial balance only includes the balance sheet accounts, such as assets, liabilities, and equity. Since all income statement accounts (revenues and expenses) have been closed out, the post-closing trial balance ensures that the ledger accounts are properly carried forward into the new accounting period.

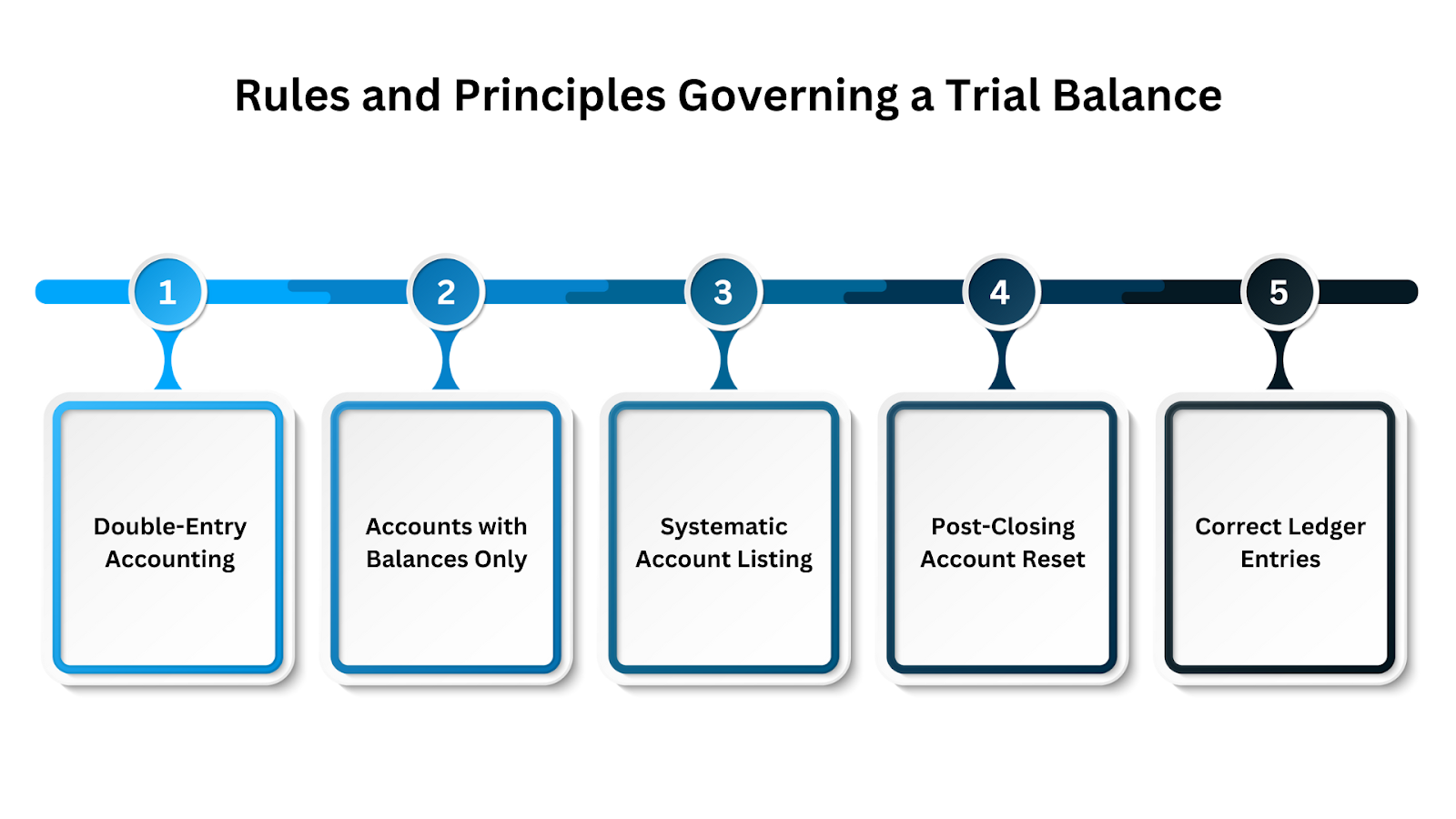

With a better understanding of the different types of trial balances, let’s look at the rules and principles that govern the preparation of a trial balance.

There are several key principles that govern the preparation of a trial balance. These ensure consistency and accuracy in the process. Some of the fundamental rules include:

Also Read: Understanding Debits and Credits in Accounting

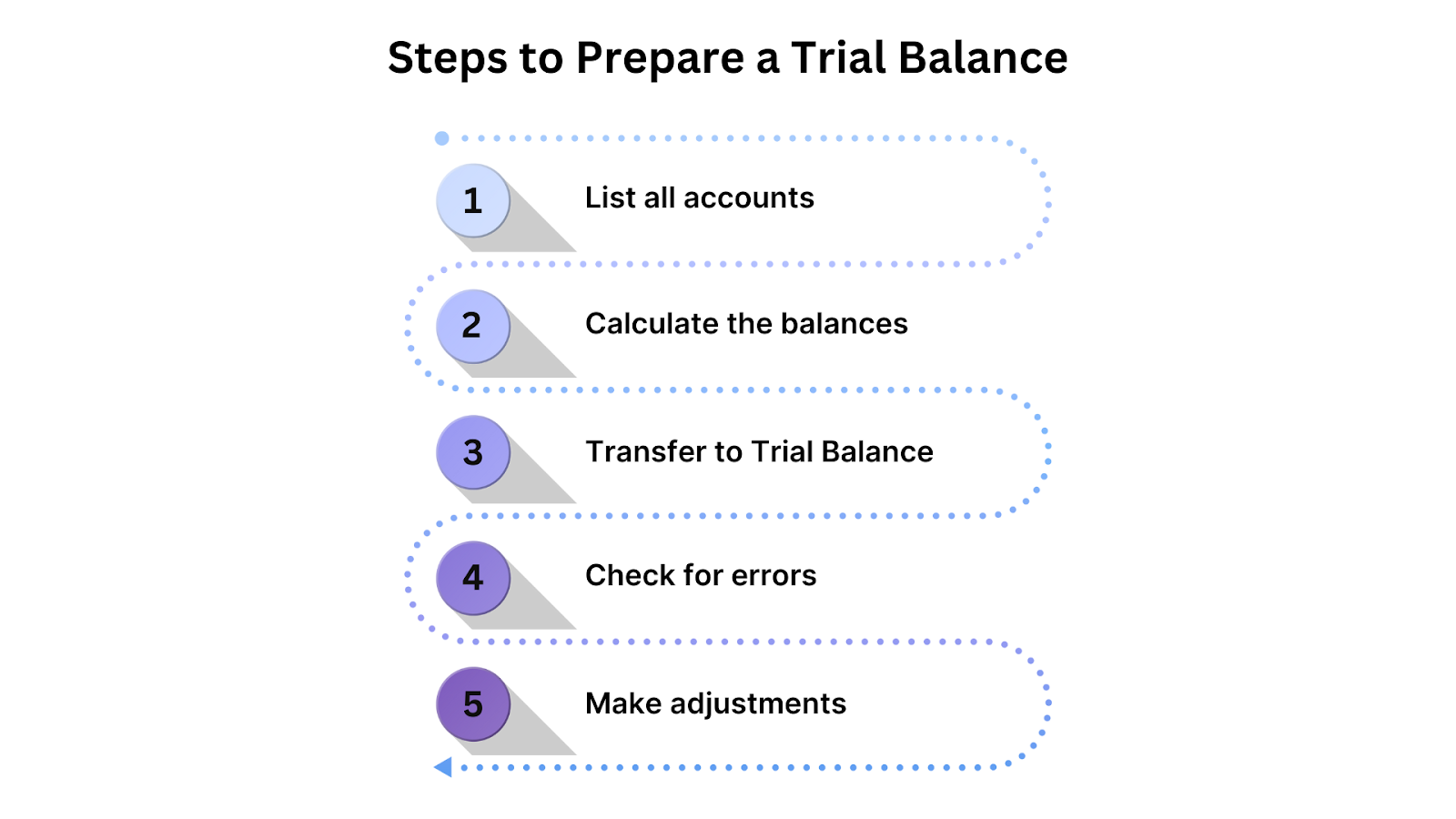

Now that we've covered the rules, let's discuss the steps involved in preparing a trial balance.

Preparing a trial balance involves a straightforward process:

Also Read: 8 Steps in the Accounting Cycle Process – A Guide

Having understood how trial balances are prepared, let’s now examine the format along with an example to gain a better comprehension.

The trial balance is an essential part of the accounting process, providing a summary of all the ledger accounts at a given point in time. It is prepared to ensure that the total debits equal the total credits, verifying the accuracy of the financial entries. Here’s the standard format of a trial balance:

The trial balance must always balance, meaning the total for the debit column must equal the total for the credit column. If this balance is maintained, it ensures that the accounting records are correct and any errors in recording have been appropriately identified.

Let’s look at a practical example to see how the trial balance is prepared and how the balances are verified.

As of 31st December 2024, XYZ Enterprises recorded the following balances after closing its general ledger accounts:

The trial balance for XYZ Enterprises, as of 31st December 2024, would be prepared as follows:

XYZ Enterprises

Trial Balance as of 31st December 2023

As shown in the example, the total debit and credit balances are equal, confirming the accuracy of the accounts and providing a reliable foundation for financial reporting.

Also Read: Saudi Businesses Rejoice! HAL Accounting Software Is Here To Revolutionize Your Finances

Now that we know what a trial balance looks like, let’s understand the advantages and disadvantages of using a trial balance in accounting.

This comparison table highlights the key advantages and disadvantages of using a trial balance, helping businesses understand its practical implications within the accounting process.

While these pros and cons apply broadly, the impact of trial balance challenges often depends on the industry in which a business operates.

While the trial balance serves the same fundamental purpose across businesses, the way it is applied varies widely by industry. Each sector in Saudi Arabia faces its own set of challenges due to the nature of its operations, regulatory environment, and financial reporting needs.

Contracting companies manage multiple projects simultaneously, often across different sites. Trial balances in this sector must account for:

Errors or delays in trial balance preparation can distort project profitability and hinder compliance reporting. For example, one construction firm reduced error detection time by 75% by using real-time trial balance dashboards in HAL ERP, allowing faster reconciliation and more accurate WIP reporting.

Trading businesses often operate across regions and currencies, which adds complexity to their trial balances. Common challenges include:

When trial balances are delayed, cost visibility and margin analysis suffer. A good example is Masader, a distributor of engineering products, which simplified trial balance and other accounting processes, allowed them to generate branch-level consolidations within seconds.

Retail businesses face unique pressures due to the sheer volume of daily transactions. Trial balances here must address:

If trial balances lag behind, compliance penalties and inaccurate profit reporting during peak sales periods can result. For instance, Al Haram, operating eight retail outlets in Saudi Arabia, achieved seamless e-invoicing compliance by integrating a tighter trial balance into POS data with HAL.

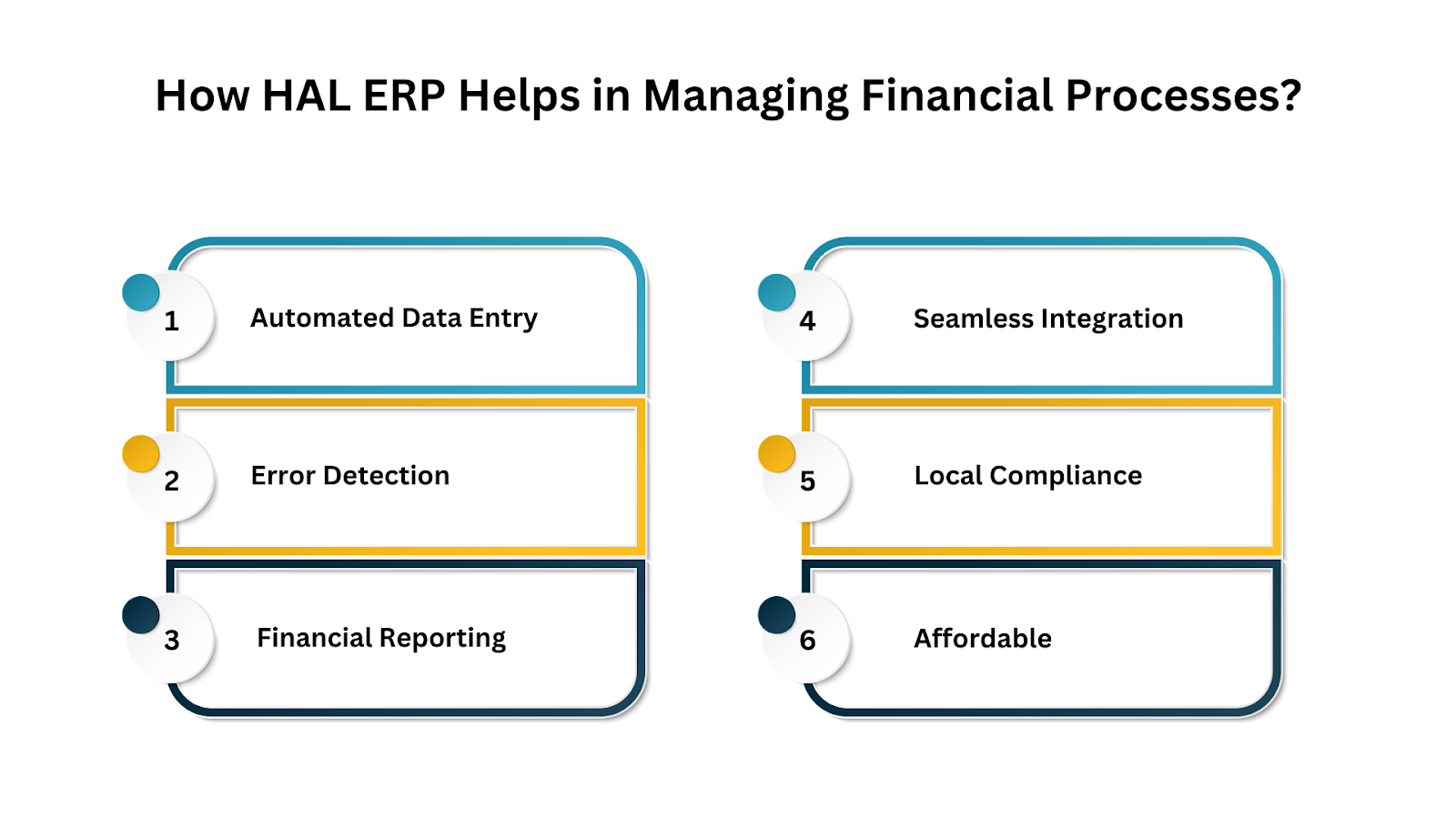

While the nature of trial balance issues varies by industry, the requirement for clarity and reliability in financial records is universal. HAL ERP helps businesses achieve this with features designed for everyday accounting needs.

HAL ERP simplifies financial management by automating entries, tracking transactions, and preparing accurate reports while ensuring compliance with ZATCA e-invoicing mandates, asset lifetimes, and asset categorisation. It also aligns with SOCPA standards, automating trial balance entries to help Saudi businesses maintain accuracy, consistency, and full regulatory compliance with less manual effort.

Here’s how HAL ERP supports businesses:

HAL ERP has enabled many businesses in Saudi Arabia to streamline their financial management. Learn how other companies have benefited from these powerful features by checking out our success stories.

The trial balance is a vital tool in accounting, providing a foundation for preparing accurate financial statements. It ensures that the accounting records are balanced and accurate, helping businesses identify and correct errors early in the process. By automating the preparation of trial balances, businesses can improve accuracy, save time, and ensure compliance with financial standards.

Explore how HAL ERP can optimize your trial balance management today. Book a demo to see how HAL ERP can streamline your accounting processes and improve your financial reporting.